How to Create a Personal Finance Plan for Beginners: A Step-by-Step Guide

Starting your financial journey can feel overwhelming, but creating a personal finance plan for beginners doesn’t have to be complicated. Whether you’re fresh out of college, starting your first job, or simply ready to take control of your money, a solid financial plan is your roadmap to financial freedom.

The statistics are sobering: nearly 60% of Americans live paycheck to paycheck, and less than 40% have enough savings to cover a $1,000 emergency. But here’s the good news—you don’t need to be a financial expert or earn a six-figure salary to turn things around. What you need is a clear plan and the commitment to follow through.

In this comprehensive guide, we’ll walk you through exactly how to create a personal finance plan that works for your unique situation, helping you build wealth, reduce stress, and achieve your financial goals. Let’s transform your financial future together, one step at a time.

What Is a Personal Finance Plan and Why Do You Need One?

Understanding Personal Finance Planning

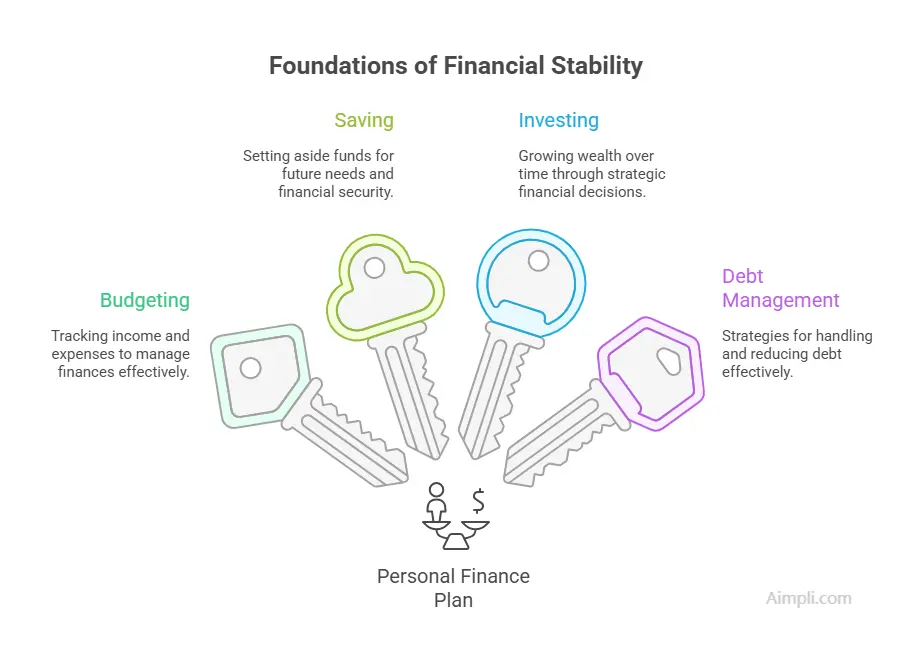

A personal finance plan is your comprehensive roadmap for managing your money effectively. Think of it as a GPS for your financial life—it tells you where you are now, where you want to go, and the best route to get there. Unlike simply “being good with money” or trying to spend less, a formal financial plan provides structure, accountability, and measurable milestones.

At its core, a personal finance plan encompasses four key components: budgeting (controlling your cash flow), saving (building financial security), investing (growing your wealth), and debt management (eliminating financial burdens). These elements work together synergistically—your budget creates room for savings, your savings provide security while tackling debt, and eliminating debt frees up money for investing.

The psychology behind financial planning is equally important. Research shows that people who write down their goals are 42% more likely to achieve them. When you create a financial plan, you’re not just organizing numbers—you’re rewiring your brain to make better money decisions. You shift from reactive spending to proactive planning, from financial anxiety to financial confidence.

Benefits of Having a Financial Plan

The benefits of creating a personal finance plan extend far beyond your bank account. First and foremost, a solid plan dramatically reduces financial stress and anxiety. When you know exactly where your money is going and have a strategy for the future, the constant worry about making ends meet begins to fade. You sleep better at night knowing you’re prepared for emergencies and working toward your goals.

A financial plan provides a clear path to achieving your dreams, whether that’s buying a home, traveling the world, starting a business, or retiring comfortably. Instead of vague wishes, you have concrete steps to follow. This clarity leads to better decision-making with money—you can quickly evaluate whether a purchase aligns with your goals or derails your progress.

Over time, following a financial plan improves your credit score as you pay bills on time, reduce debt, and demonstrate financial responsibility. A better credit score opens doors to lower interest rates on loans, better insurance premiums, and even improved job prospects in some fields.

Perhaps most importantly, a personal finance plan lays the foundation for long-term wealth building. Compound interest and consistent investing work their magic when you have a plan and stick to it. What starts as small monthly contributions can grow into substantial wealth over decades, providing financial independence and the freedom to live life on your terms.

Step 1: Assess Your Current Financial Situation

Before you can plot a course to financial success, you need to know your starting point. This crucial first step involves taking an honest, comprehensive look at your current financial situation. While it might feel uncomfortable to confront the reality of your finances, remember that awareness is the first step toward improvement.

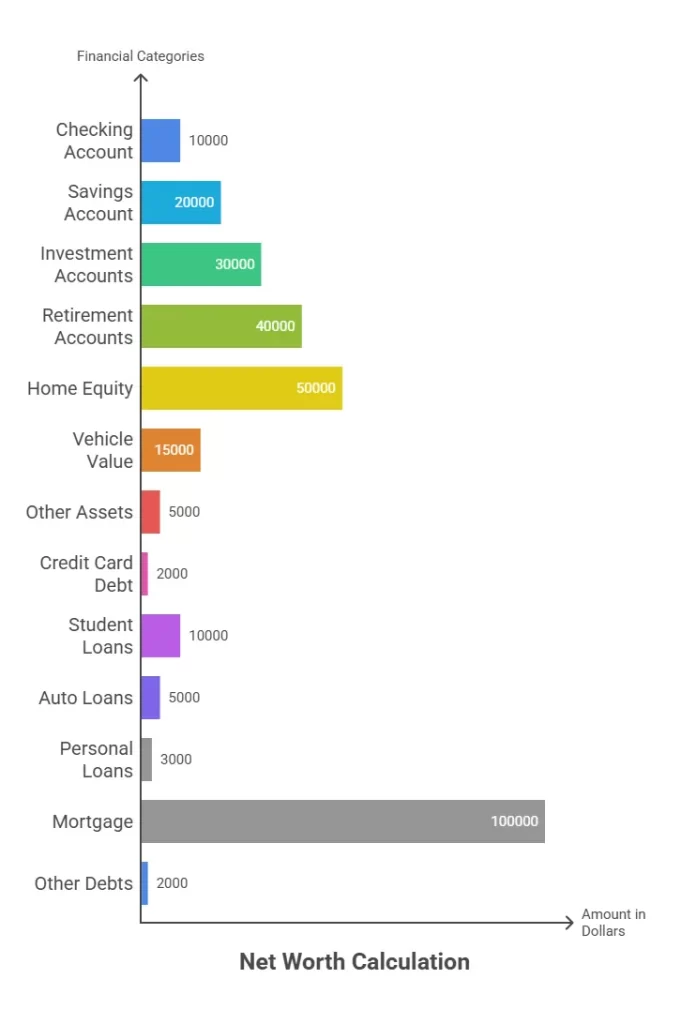

Calculate Your Net Worth

Your net worth is the most fundamental measure of your financial health. It’s calculated using a simple formula: Assets minus Liabilities equals Net Worth. Assets include everything you own that has monetary value—bank account balances, investment accounts, retirement funds, real estate equity, and valuable possessions like vehicles. Liabilities encompass all your debts—credit card balances, student loans, car loans, personal loans, and mortgage debt.

To calculate your net worth, start by listing all your assets with their current values. Check your bank statements, investment account balances, and retirement account statements. For your home or car, use realistic market values, not what you paid or what you hope they’re worth. Next, list all your liabilities with their current balances. Don’t forget about smaller debts like medical bills or money owed to family members.

Here’s an important reality check for beginners: having a negative net worth is completely normal, especially if you have student loans or recently financed a car. What matters isn’t where you start, but the direction you’re heading. Your goal is to see this number increase over time as you pay down debt and build assets.

Analyze Your Income and Expenses

Understanding your cash flow—the money coming in and going out each month—is essential for creating a realistic financial plan. Start by calculating your total monthly income after taxes. Include your salary, any side hustle income, investment dividends, rental income, or other regular money sources. Use your take-home pay, not your gross salary, since you can’t spend money that goes to taxes and benefits.

Next comes the eye-opening part: tracking your expenses. Most people significantly underestimate how much they spend. Categorize your expenses into fixed costs (rent or mortgage, car payment, insurance, subscriptions) and variable costs (groceries, dining out, entertainment, shopping). Fixed expenses stay relatively constant each month, while variable expenses fluctuate.

For the most accurate picture, review three months of bank and credit card statements. Categorize every transaction. Yes, every single one. Those daily coffee runs add up to over $100 per month. That forgotten streaming subscription you never use still costs $15 monthly. These small expenses are often where money mysteriously disappears.

Modern technology makes tracking easier than ever. Apps like Mint automatically categorize your spending by connecting to your bank accounts. YNAB (You Need A Budget) helps you plan ahead with zero-based budgeting. Personal Capital provides a comprehensive view of your entire financial picture, including investments. Choose a tool that fits your style and commit to using it consistently.

As you analyze your spending patterns, look for trends and problem areas. Do you overspend on weekends? Does online shopping spike when you’re stressed? Are you spending 50% of your income on housing when the recommended maximum is 30%? Identifying these patterns helps you make targeted improvements rather than vague promises to “spend less.”

Review Your Credit Report

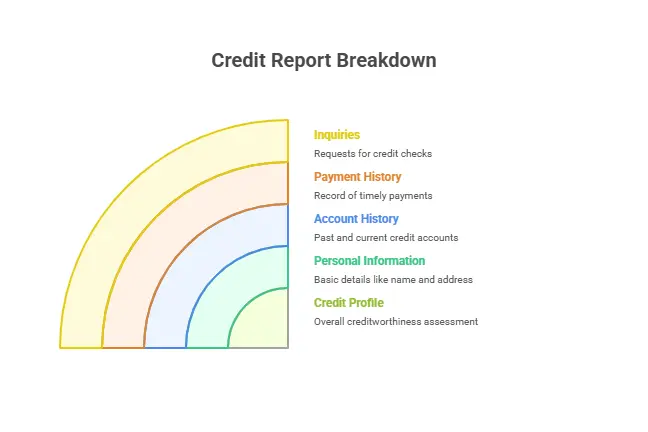

Your credit report is like your financial report card, and checking it regularly is crucial for your financial health. By law, you’re entitled to one free credit report annually from each of the three major credit bureaus—Equifax, Experian, and TransUnion—through AnnualCreditReport.com. This is the only truly free and official source for credit reports.

When you review your credit report, you’re looking for several things. First, verify that all information is accurate. Check that accounts listed actually belong to you, balances are correct, and payment history is accurate. Errors on credit reports are surprisingly common—studies show that one in five people have errors that could negatively impact their credit score.

Your credit score, which ranges from 300 to 850, is calculated based on factors in your credit report: payment history (35%), amounts owed (30%), length of credit history (15%), new credit (10%), and credit mix (10%). Understanding these factors helps you make strategic decisions to improve your score over time.

If you spot errors, dispute them immediately. Each credit bureau has an online dispute process. Provide documentation supporting your claim, and the bureau must investigate within 30 days. Correcting errors can sometimes boost your credit score by 50 points or more.

Why does credit matter for your financial future? Your credit score affects your ability to borrow money and the interest rates you’ll pay. A score above 740 typically qualifies you for the best rates on mortgages and auto loans, potentially saving you tens of thousands of dollars over the life of a loan. Credit also influences insurance premiums, rental applications, and even some job opportunities. Building and maintaining good credit is a cornerstone of long-term financial success.

Step 2: Set Clear Financial Goals

With a clear understanding of your current financial situation, it’s time to define where you want to go. Setting specific, measurable financial goals transforms vague aspirations into actionable plans. Your goals become the “why” that motivates you to stick with your financial plan when temptation strikes.

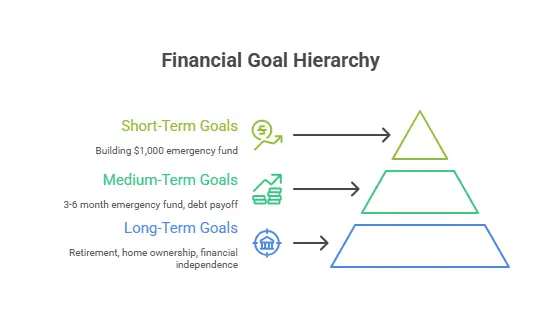

Short-Term Goals (0-2 years)

Short-term goals provide quick wins that build momentum and confidence. These are objectives you can achieve relatively quickly, keeping you motivated on your financial journey.

Building a $1,000 emergency fund should be your first priority. This starter fund protects you from going deeper into debt when unexpected expenses inevitably arise. Whether it’s a car repair, medical copay, or broken appliance, having $1,000 set aside means you can handle it without reaching for a credit card.

Paying off high-interest credit card debt is another crucial short-term goal. Credit cards charging 20% or more in annual interest are financial quicksand—the longer you carry the balance, the harder it becomes to escape. Eliminating this debt frees up cash flow and stops you from throwing money away on interest.

Saving for a vacation or large purchase provides positive motivation. Financial plans work best when they balance delayed gratification with present enjoyment. Planning for something fun keeps your financial journey from feeling like pure deprivation.

Creating a monthly budget you can actually stick to is a foundational short-term goal. Many people create overly restrictive budgets that fail within weeks. Your goal should be developing a realistic, sustainable budget that aligns with your values and priorities.

Medium-Term Goals (2-5 years)

Medium-term goals bridge the gap between immediate needs and long-term dreams. These objectives require sustained effort and discipline but deliver substantial improvements to your financial security.

Establishing a full emergency fund covering three to six months of expenses is a medium-term priority after paying off high-interest debt. This robust safety net protects you from job loss, extended illness, or major unexpected expenses without derailing your financial progress. The exact target depends on your circumstances—six months is better if you’re self-employed, have variable income, or work in an unstable industry.

Saving for a down payment on a house is a common medium-term goal. While the traditional 20% down payment reduces your monthly mortgage and eliminates private mortgage insurance, even 5-10% down can get you into a home with certain loan programs. Start researching home prices in your target area and calculate how much you need to save monthly to reach your goal.

Paying off student loans or car loans eliminates monthly obligations and frees up hundreds of dollars in cash flow. While some financial experts debate whether to aggressively pay off low-interest debt, eliminating these payments provides psychological benefits and financial flexibility.

Starting to invest in retirement accounts, even modestly, allows compound interest to begin working its magic. Thanks to time value of money, a small amount invested in your twenties grows exponentially more than a larger amount invested later.

Long-Term Goals (5+ years)

Long-term goals shape your overall financial future and require decades of consistent effort. These are the objectives that transform your financial life and provide true wealth and security.

Retirement planning should be every working person’s primary long-term goal. Maximizing 401(k) contributions, especially to capture full employer matching, accelerates your retirement savings. The general rule suggests saving 15% of your gross income for retirement, though starting with any amount is better than waiting.

College savings for children, typically through 529 plans, helps ensure your kids aren’t burdened with massive student debt. Starting early allows investments to grow substantially over 18 years. Even $100 monthly from birth can grow to over $40,000 by college age with average returns.

Paying off your mortgage completely provides unparalleled financial freedom. Imagine retirement without a house payment—how much less money would you need? While low mortgage interest rates make this goal less urgent, the psychological benefit of owning your home outright is immense.

Achieving financial independence—having enough passive income and assets to cover living expenses without working—represents the ultimate long-term goal. This might mean traditional retirement at 65, or it could mean “Financial Independence, Retire Early” (FIRE) in your forties or fifties.

Making Goals SMART

Simply writing “save more money” or “get out of debt” isn’t enough. Effective financial goals follow the SMART framework: Specific, Measurable, Achievable, Relevant, and Time-bound.

Specific goals clearly define what you want to accomplish. “Pay off debt” is vague. “Pay off my $5,000 credit card balance” is specific.

Measurable goals include numbers so you can track progress. “Save for emergencies” becomes “Save $1,000 for my starter emergency fund.”

Achievable goals are realistic given your income and expenses. Setting a goal to save $2,000 monthly when you only earn $3,000 sets you up for failure. Better to start with $200 monthly and increase over time.

Relevant goals align with your values and priorities. Don’t save for a house down payment if you prefer renting and traveling. Your goals should excite and motivate you.

Time-bound goals have clear deadlines. “Pay off $5,000 credit card debt by December 31, 2026” creates urgency and allows you to calculate required monthly payments ($208 monthly for 24 months).

Transform “I want to buy a house someday” into “I will save $30,000 for a down payment by January 2028 by saving $850 monthly in a high-yield savings account.” That’s a SMART goal that provides a clear roadmap.

Step 3: Create a Realistic Budget

A budget is simply a plan for your money—it tells every dollar where to go instead of wondering where it went. Despite budgeting’s reputation as restrictive or boring, a well-designed budget actually provides freedom. When you control your money intentionally, you eliminate the anxiety of not knowing if you can afford something.

Choose a Budgeting Method

Different budgeting methods work for different personalities and situations. The key is finding one that fits your lifestyle and mindset so you’ll actually stick with it.

The 50/30/20 Rule is the simplest method for beginners. Popularized by Senator Elizabeth Warren, this approach allocates 50% of your after-tax income to needs (housing, utilities, groceries, insurance, minimum debt payments), 30% to wants (dining out, entertainment, hobbies, travel), and 20% to savings and extra debt payments. This method provides structure without requiring detailed tracking of every expense category.

Zero-based budgeting gives every dollar a job. Your income minus all planned expenses, savings, and debt payments should equal zero. This doesn’t mean spending everything—savings and investments are “expenses” in this system. YNAB (You Need A Budget) software is built around this philosophy. Zero-based budgeting provides maximum control and awareness but requires more time and discipline.

The Envelope System uses physical cash divided into envelopes for different spending categories. When an envelope is empty, you stop spending in that category until the next month. This tactile approach makes spending feel real in a way that swiping cards doesn’t. While using physical cash is less common today, you can replicate this digitally by maintaining separate checking accounts or using apps that create virtual envelopes.

The Pay-Yourself-First Method prioritizes savings and investments before allocating money to expenses. As soon as your paycheck deposits, automatic transfers move money to savings, retirement, and investment accounts. You then budget and spend whatever remains. This method ensures your financial goals get funded but requires discipline to live on what’s left.

For beginners, the 50/30/20 Rule typically works best. It provides structure without overwhelming detail, is flexible enough to work with various income levels, and doesn’t require sophisticated tracking tools. As you become more comfortable with budgeting, you can explore more detailed methods if desired.

Budgeting Methods Comparison

| Method | Complexity | Best For | Pros | Cons |

|---|---|---|---|---|

| 50/30/20 Rule | Low | Beginners who want simplicity | Easy to understand and implement, flexible | Less precise, may not work with very low income |

| Zero-Based | High | Detail-oriented people who want maximum control | Complete awareness of every dollar, intentional spending | Time-consuming, requires discipline |

| Envelope System | Medium | Visual learners and overspenders | Makes spending tangible, prevents overspending | Inconvenient with cash, harder to track |

| Pay-Yourself-First | Low-Medium | People who struggle to save after expenses | Prioritizes goals, builds savings automatically | Requires living on less, may create cash flow issues initially |

Build Your Monthly Budget

Creating your first budget starts with listing all income sources. Include your primary job (after-tax income), side hustle earnings, investment dividends, rental income, or any other regular money sources. Be conservative—use your lowest typical monthly income if it varies.

Next, categorize and list all expenses. Start with essential fixed expenses: rent or mortgage, utilities (electricity, water, gas, internet), insurance (health, auto, renters/homeowners), debt minimum payments, and necessary subscriptions. These expenses stay relatively constant and must be paid.

Then list essential variable expenses: groceries, gas for commuting, basic clothing, necessary household items, and childcare. These fluctuate monthly but are still necessary.

Now for discretionary spending: dining out, entertainment, hobbies, non-essential shopping, subscriptions you enjoy but don’t need, and miscellaneous purchases. This is where you have the most flexibility to cut if needed.

Finally, and most importantly, prioritize savings and debt payments beyond minimums. Include your emergency fund contributions, retirement savings, extra debt payments, and savings for specific goals. Many people make the mistake of saving “whatever’s left” at month-end—which is usually nothing. Instead, treat savings like a fixed expense that gets paid first.

Leave room for flexibility in your budget. Life happens. You’ll occasionally need to spend more on groceries during a holiday, or an unexpected expense will pop up. Build in a small “miscellaneous” category or keep your spending categories slightly conservative so unexpected costs don’t completely derail your plan.

Your income minus all expenses, savings, and debt payments should either equal zero (zero-based budgeting) or show a small surplus you can direct to goals. If your expenses exceed income, you have two options: increase income through a side hustle or better-paying job, or decrease expenses by cutting discretionary spending and finding ways to reduce fixed costs.

Track and Adjust Your Budget

Creating a budget is the easy part—following it consistently is where most people struggle. Success requires regular tracking and a willingness to adjust as needed.

Conduct weekly spending check-ins. Every Sunday, spend 10-15 minutes reviewing the past week’s transactions. How do your actual expenses compare to your budget? Are you on track, overspending in certain categories, or doing better than expected? These weekly reviews keep you aware and allow for course corrections before the month ends.

At month-end, do a comprehensive monthly budget review. Did you stick to your plan? Where did you succeed? What categories consistently go over budget? Are there expenses you forgot to budget for? Use these insights to refine next month’s budget.

Adjust for irregular expenses that don’t occur monthly. Insurance premiums might be quarterly, vehicle registration annual, and holiday shopping seasonal. Create a monthly line item for these irregular expenses, calculating the annual cost and dividing by 12. Transfer this amount to a separate savings account so the money is available when needed.

Celebrate small wins along the way. Did you come in under budget in a category? Put the difference toward a financial goal and acknowledge your success. Did you resist an impulse purchase by checking your budget first? Recognize that victory. Positive reinforcement makes budgeting feel rewarding rather than restrictive.

Use automation to simplify budgeting. Set up automatic bill pay for fixed expenses so you never miss due dates. Schedule automatic transfers to savings accounts immediately after payday so saving happens without willpower. The less you have to think about and manually manage, the more likely you’ll stick with your budget long-term.

Remember that your first budget won’t be perfect, and that’s okay. Budgeting is a skill that improves with practice. Each month, you’ll get better at estimating expenses, identifying priorities, and making intentional spending decisions. Give yourself grace during the learning process.

Here’s a sample monthly budget template:

Monthly Budget Template

| Category | Details | Allocated Amount ($) |

|---|---|---|

| Income | Salary | 3,000 |

| Freelance / Side Income | 500 | |

| Other Income | 200 | |

| Total Income | 3,700 | |

| Expenses | Rent / Mortgage | 1,000 |

| Utilities (Electricity, Water, Internet) | 250 | |

| Groceries | 400 | |

| Transportation | 200 | |

| Insurance | 150 | |

| Subscriptions / Entertainment | 100 | |

| Dining Out | 150 | |

| Miscellaneous | 100 | |

| Total Expenses | 2,350 | |

| Savings & Investments | Emergency Fund | 300 |

| Retirement Savings | 400 | |

| Investment (Stocks / Mutual Funds) | 250 | |

| Total Savings / Investments | 950 | |

| Summary | Total Income | $3,700 |

| Total Expenses | $2,350 | |

| Total Savings / Investments | $950 | |

| Remaining Balance (Income − Expenses − Savings) | $400 |

Step 4: Build Your Emergency Fund

An emergency fund is your financial safety net—cash reserves set aside specifically for unexpected expenses and financial emergencies. This fund is arguably the most important component of any personal finance plan, yet it’s what many people skip in their eagerness to invest or pay off debt faster.

Why Emergency Funds Are Essential

Life is unpredictable. Your car will eventually need repairs. You or a family member will get sick. Home appliances break. Job loss happens. Without an emergency fund, these inevitable situations force you to choose between going deeper into debt or falling behind on bills. Neither option is acceptable.

An emergency fund protects you against job loss or income reduction. If you lose your job, having three to six months of expenses saved means you can focus on finding the right next opportunity instead of desperately taking the first offer. You avoid the nightmare scenario of missing mortgage payments or facing eviction while unemployed.

Emergency funds prevent debt when unexpected expenses arise. When your transmission fails and the repair costs $2,000, having the cash available means you pay the mechanic and move on with life. Without savings, you’re forced to put it on a credit card at 20% interest, turning a one-time expense into months of debt payments.

The psychological benefits of emergency savings are equally important. Financial stress affects health, relationships, work performance, and overall quality of life. Knowing you have a cushion provides peace of mind and financial confidence. You sleep better at night. You’re less anxious about money. You can make better long-term decisions instead of constantly operating in crisis mode.

The statistics are alarming: according to Federal Reserve data, nearly 40% of Americans couldn’t cover a $400 emergency expense without borrowing or selling something. Don’t be part of that statistic. Building an emergency fund transforms you from financially fragile to financially resilient.

How Much to Save

The recommended emergency fund size depends on your personal circumstances, but general guidelines provide a starting point.

Your first milestone is a starter emergency fund of $500 to $1,000. This isn’t enough to cover job loss, but it handles most small emergencies—a car repair, urgent care visit, or broken appliance. Prioritize this starter fund before aggressively paying down debt (except payday loans or other predatory debt). Having this cushion prevents you from going further into debt when life happens.

After paying off high-interest debt, build your full emergency fund covering three to six months of essential expenses. Note that this is expenses, not income. Calculate your monthly needs for housing, utilities, food, transportation, insurance, and minimum debt payments. Multiply by 3-6 to get your target.

Several factors affect whether you should lean toward three months or six months of savings. Choose the higher end if you’re self-employed or have variable income, work in an unstable industry or company, have dependents relying on your income, have chronic health issues, are the sole earner in your household, or own a home (more can go wrong requiring expensive repairs).

Choose three months if you’re in a stable job with strong demand for your skills, have dual income in your household, have minimal debt and expenses, rent rather than own (landlord covers major repairs), or have strong family support as a backup safety net.

Some people wonder if they should have even more than six months saved. Generally, no—beyond six months, you’re better off investing that money for growth rather than keeping it in low-interest savings. The opportunity cost of keeping too much in cash savings can be significant over time.

Where to Keep Your Emergency Fund

Emergency fund money must be safe, easily accessible, and separate from your regular checking account, but it shouldn’t be invested in stocks or other volatile assets.

High-yield savings accounts are ideal for emergency funds. Online banks like Ally, Marcus by Goldman Sachs, and Discover typically offer interest rates significantly higher than traditional brick-and-mortar banks—often 4-5% compared to 0.01% at big banks. Your money is FDIC insured up to $250,000, earns reasonable interest while it sits, and remains easily accessible through electronic transfer (usually 1-3 business days).

Money market accounts function similarly to high-yield savings but sometimes offer slightly higher rates or come with check-writing privileges. Ensure any money market account is FDIC insured (some investment money market funds are not).

What should you avoid? Don’t invest emergency funds in stocks, bonds, or other volatile investments. You need guaranteed access to your full amount when emergencies strike—you can’t wait for the market to recover from a downturn. Don’t keep your emergency fund in regular checking where it’s too tempting to spend on non-emergencies. Don’t use certificates of deposit (CDs) that lock up your money, though laddering shorter-term CDs can work for a portion of a large emergency fund.

As of late 2024 and early 2025, high-yield savings account rates remain relatively attractive following the Federal Reserve’s rate increases. Shop around—rates vary significantly between banks and change over time. Websites like Bankrate and NerdWallet track current top rates.

Building Your Fund Step-by-Step

Building an emergency fund from zero feels daunting, but consistent small contributions add up faster than you think.

Start small if necessary. Even $25 per paycheck reaches $650 in a year. That’s halfway to a $1,000 starter fund. If you’re paid biweekly, $50 per check reaches $1,300 annually. Find an amount that feels achievable and commit to it.

Automate transfers to savings immediately after payday. Set up your direct deposit to split between checking and savings, or schedule automatic transfers. Remove the temptation and decision-making—make saving automatic and effortless.

Use financial windfalls to jump-start your emergency fund. Tax refunds, work bonuses, gifts, or inheritances can instantly boost your savings. While it’s tempting to spend windfall money on something fun, using at least half for your emergency fund fast-forwards your financial security by months or years.

Temporarily cut unnecessary expenses to build your fund faster. That $15 monthly subscription you rarely use equals $180 annually toward emergencies. Skipping daily coffee shop visits could save $100 monthly or $1,200 yearly. Look for painless cuts—expenses you won’t really miss but that free up cash for your fund.

Challenge yourself with no-spend days, weeks, or months. A no-spend challenge means buying nothing beyond essentials for a set period. All the money you would have spent on discretionary items goes to your emergency fund instead. These challenges highlight how much you normally spend without thinking and can dramatically accelerate your savings.

Remember that building an emergency fund is a marathon, not a sprint. It might take 12-24 months to fully fund three to six months of expenses, and that’s okay. Every dollar you save increases your financial security and resilience. Stay consistent, trust the process, and celebrate milestones along the way.

Step 5: Tackle High-Interest Debt

Debt is one of the biggest obstacles to financial success. High-interest debt specifically—credit cards, payday loans, and other expensive borrowing—actively sabotages your financial progress by draining hundreds or thousands of dollars in interest annually.

Understanding Different Types of Debt

Not all debt is created equal. Understanding the difference between types helps you prioritize your payoff strategy.

“Good debt” finances assets that increase in value or generate income: mortgages (home typically appreciates), student loans (education increases earning potential), and business loans (business generates profit). These debts usually have lower interest rates and potential tax benefits. While being debt-free is always preferable, good debt can be a reasonable financial tool when used wisely.

“Bad debt” finances depreciating assets or consumption: credit card balances (especially from everyday spending), auto loans (cars lose value), personal loans for vacations or weddings, and payday loans. These debts typically carry higher interest rates and provide no financial return.

Interest rates determine debt priority. Credit cards often charge 15-25% APR or higher. At 20% interest, a $5,000 balance costs $1,000 annually just in interest. Personal loans might charge 10-15%. Auto loans typically range from 4-10% depending on credit. Student loans are often 4-7%. Mortgages are usually 3-7%.

As a rule of thumb, debt charging over 7-8% interest is “high-interest debt” that should be aggressively paid off before focusing on investing. The guaranteed “return” of eliminating 20% interest debt exceeds what you can reasonably expect from investments.

Compound interest works against you with debt, especially when you only make minimum payments. A $3,000 credit card balance at 18% interest with minimum payments of 2% takes over 30 years to pay off and costs nearly $5,000 in interest. The same balance paid off in 18 months costs only $500 in interest. Time is expensive with debt.

Debt Repayment Strategies

Two proven strategies help you systematically eliminate debt: the debt snowball and debt avalanche methods. Both work—choose the one that fits your personality.

The debt snowball method ranks debts from smallest to largest balance, ignoring interest rates. You make minimum payments on everything, then put all extra money toward the smallest debt. When that’s paid off, roll that payment to the next smallest debt, creating a growing payment “snowball.” This method provides quick psychological wins. Paying off that first debt—even if it’s small—feels amazing and motivates you to keep going. The momentum and emotional boost often help people stick with debt payoff longer.

The debt avalanche method ranks debts from highest to lowest interest rate, ignoring balance sizes. You make minimum payments on everything, then attack the highest-interest debt with all extra funds. When that’s eliminated, roll the payment to the next highest-interest debt. This method saves the most money in interest and pays off debt faster mathematically. If you’re motivated by numbers and optimization rather than quick wins, this is your method.

Debt Payoff Comparison: Snowball vs. Avalanche

| Method | Order of Payment | Total Time to Debt Free | Total Interest Paid | First Debt Payoff | Psychological Boost | Money Saved |

|---|---|---|---|---|---|---|

| Snowball | Card 1 ($1,000, 15% APR) → Card 2 ($4,000, 20% APR) → Card 3 ($10,000, 18% APR) | 48 months | $3,200 | 3 months | HIGH | – |

| Avalanche | Card 2 ($4,000, 20% APR) → Card 3 ($10,000, 18% APR) → Card 1 ($1,000, 15% APR) | 45 months | $2,800 | 12 months | MEDIUM | $400 |

Debt consolidation combines multiple debts into a single loan, ideally at a lower interest rate. A personal consolidation loan, balance transfer credit card (often 0% intro APR for 12-18 months), or home equity loan can simplify payments and reduce interest. However, consolidation doesn’t reduce the amount owed—it just restructures it. Be cautious of extending loan terms so far that you pay more interest overall, and address the underlying spending behaviors that created the debt.

Balance transfer credit cards offering 0% introductory APR can be powerful debt payoff tools. Transferring a $5,000 balance from 20% interest to 0% for 15 months saves hundreds in interest if you aggressively pay down the principal. However, be aware of balance transfer fees (typically 3-5%) and ensure you pay off the balance before the promotional period ends—remaining balances usually jump to high regular rates.

Staying Motivated During Debt Payoff

Paying off significant debt takes time—often years. Staying motivated through the journey requires strategy and mindset shifts.

Track your progress visually using charts, apps, or debt payoff trackers. Seeing the balances decrease and watching your progress bar fill provides tangible evidence of your hard work. Many people find coloring in a thermometer chart or crossing off milestones particularly satisfying.

Celebrate milestones along the way. Paid off your first debt? Celebrate with a modest, budget-friendly reward like a movie night at home or favorite meal. Reduced total debt by 25%? Have a small celebration that acknowledges your dedication. These celebrations make the journey feel less like pure deprivation.

Find free or low-cost entertainment during your intense debt payoff phase. Explore free community events, host game nights instead of expensive dinners out, use your library for books and movies, enjoy free outdoor activities like hiking or parks, and take advantage of free museum days. Living frugally doesn’t mean living miserably—it means being creative and intentional.

Avoid taking on new debt while paying off existing debt. This seems obvious but is where many people sabotage their progress. Cut up credit cards if you can’t resist using them (you can still pay them off without the physical card). Develop strategies to handle impulse spending urges—wait 24-48 hours before buying, remove shopping apps from your phone, or use cash-only for discretionary spending.

Connect with others on the same journey. Online communities, debt-free Facebook groups, and local financial peace groups provide support, accountability, and encouragement. Knowing you’re not alone and hearing others’ success stories fuels your motivation during difficult moments.

Remember your “why”—the reason you’re making these sacrifices. Maybe it’s buying a home, starting a family without financial stress, career flexibility, or simply peace of mind. Write down your why and review it when motivation wanes. Your future debt-free self will thank you for the temporary sacrifices.

Step 6: Start Investing for the Future

Once you’ve built your emergency fund and tackled high-interest debt, it’s time to shift focus toward building long-term wealth through investing. This is where your money starts working for you instead of you working for every dollar.

Why Beginners Need to Invest

The power of compound interest is the closest thing to magic in personal finance. Albert Einstein allegedly called it “the eighth wonder of the world,” saying “he who understands it, earns it; he who doesn’t, pays it.” When you invest, your money earns returns. Those returns then earn returns. Over decades, this compounding effect creates exponential growth.

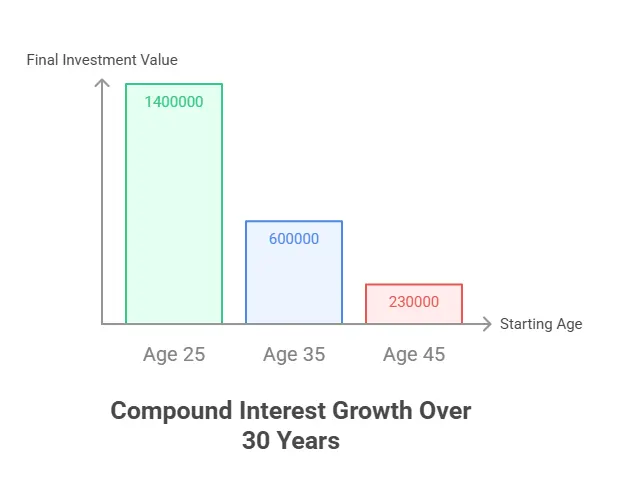

Consider this example: If you invest $500 monthly starting at age 25 with an average 8% annual return, you’ll have approximately $1.4 million by age 65. Wait until age 35 to start, and you’ll have only $600,000—less than half, despite only a 10-year delay. Start at 45, and you’ll have just $230,000. Time is your most valuable investing asset.

Investing is essential for beating inflation. Inflation erodes purchasing power over time—what costs $100 today might cost $180 in 20 years at 3% annual inflation. Money sitting in a regular savings account earning 0.01% interest actively loses value in real terms. Investments averaging 7-10% annually maintain and grow your purchasing power.

The “time in the market vs. timing the market” principle is crucial for beginners to understand. Trying to predict market highs and lows to buy and sell at perfect times is essentially impossible, even for professionals. Research consistently shows that staying invested through market ups and downs produces better results than trying to time entries and exits. Missing just the 10 best days in the market over 20 years can reduce returns by 50% or more.

Starting small is infinitely better than not starting at all. Some people delay investing because they think they need thousands of dollars to begin. Modern investing platforms allow you to start with as little as $5-10. Contributing $50 monthly is better than waiting until you can afford $500. The habit and compound interest clock matter more than the initial amount.

Retirement Accounts for Beginners

Retirement accounts offer significant tax advantages that accelerate wealth building. Understanding your options helps you choose the best vehicles for your situation.

A 401(k) is an employer-sponsored retirement plan that lets you contribute pre-tax dollars directly from your paycheck. Your contributions reduce your taxable income—contributing $10,000 annually could save $2,200 in taxes if you’re in the 22% tax bracket. The money grows tax-deferred, meaning you pay no taxes on investment gains until retirement withdrawals. In 2024-2025, you can contribute up to $23,000 annually ($30,500 if age 50+).

The absolute best investment available to most people is the employer 401(k) match. If your employer matches 50% of contributions up to 6% of salary, that’s an immediate 50% return—guaranteed. Someone earning $50,000 contributing 6% ($3,000) receives $1,500 in free money. Never leave employer match money on the table. Contribute at least enough to capture the full match before focusing elsewhere.

Individual Retirement Accounts (IRAs) come in two main flavors: Traditional and Roth. Both allow $7,000 annual contributions in 2024-2025 ($8,000 if age 50+), but the tax treatment differs.

Traditional IRAs offer tax deductions today—contributions reduce current taxable income. Money grows tax-deferred, and you pay taxes on withdrawals in retirement. This works well if you expect to be in a lower tax bracket during retirement than you are now.

Roth IRAs use after-tax dollars—no deduction today—but all growth and withdrawals in retirement are completely tax-free. This is powerful if you expect to be in a higher tax bracket later or want tax-free income flexibility in retirement. Roth IRAs also allow you to withdraw contributions (not earnings) anytime without penalty, providing some emergency accessibility.

For most beginners, the recommended approach is: contribute enough to your 401(k) to get the full employer match, then fully fund a Roth IRA ($7,000), then return to maxing your 401(k) if you have more to invest. This strategy captures free employer money while prioritizing tax-free Roth growth.

Investment Basics

The investing world can seem overwhelmingly complex, but beginners need to understand just a few core concepts to succeed.

Index funds are mutual funds or ETFs that track a market index like the S&P 500 (500 largest US companies). Instead of trying to pick winning individual stocks, you own a tiny piece of hundreds or thousands of companies. Index funds offer instant diversification, low costs (expense ratios often 0.03-0.15%), and historically strong returns averaging 9-10% annually over long periods. For most beginners, a simple portfolio of index funds covering US stocks, international stocks, and bonds is completely sufficient.

Asset allocation means dividing investments between different asset classes—stocks, bonds, and cash. Stocks offer higher growth potential with more volatility. Bonds provide stability and income with lower returns. A common rule of thumb is subtracting your age from 110 to determine your stock percentage (a 30-year-old would hold 80% stocks, 20% bonds). Younger investors can handle more stock volatility because they have decades to recover from market downturns.

Diversification means not putting all eggs in one basket. Instead of investing everything in your employer’s stock or a single industry, you spread risk across many companies, sectors, and asset classes. Index funds provide instant diversification—owning the S&P 500 index means you’re invested in technology, healthcare, finance, consumer goods, and every other major sector.

Dollar-cost averaging is simply investing the same amount regularly regardless of market conditions. Instead of trying to time the market, you invest $500 every month whether stocks are up or down. This strategy removes emotion, ensures consistent investing, and actually benefits from volatility—you automatically buy more shares when prices are low and fewer when prices are high.

Robo-advisors like Betterment, Wealthfront, or Vanguard Digital Advisor offer automated investment management for low fees (typically 0.25-0.50% annually). You answer questions about your goals and risk tolerance, and the platform builds and manages a diversified portfolio using low-cost index funds. This is excellent for beginners who want professional management without high costs or minimum balances.

DIY investing through brokerages like Vanguard, Fidelity, or Schwab gives you complete control to choose your own investments. This works well if you’re comfortable with basic investment concepts and prefer a simple index fund portfolio. Modern platforms make DIY investing straightforward with no trading commissions and low minimums.

Common investing mistakes beginners should avoid include: trying to pick individual stocks without knowledge or experience, panic selling during market downturns, checking investments too frequently and reacting emotionally, paying high fees for actively managed funds that underperform index funds, keeping too much money in cash earning minimal interest, and failing to rebalance portfolios periodically.

How Much Should You Invest?

The popular 15% retirement savings rule suggests investing 15% of your gross income for retirement. Someone earning $60,000 should invest $9,000 annually ($750 monthly). This includes employer contributions—if your employer matches $3,000, you need to contribute $6,000 yourself.

Starting at 15% from your first job theoretically provides a comfortable retirement, but this isn’t always realistic for beginners. Start with whatever you can afford—even 5%—and increase by 1-2% annually. Many employers offer automatic contribution increases tied to raises, making this painless.

The question of balancing investing with debt payoff depends on interest rates. As mentioned earlier, aggressively pay off debt exceeding 7-8% interest before investing beyond the employer match. For lower-interest debt like mortgages or student loans below 5%, it often makes sense to make minimum payments while investing for the long-term growth potential.

Increase contributions over time as your income grows. When you get a raise, direct at least half toward increased retirement savings before lifestyle inflation consumes it. A 3% raise could mean increasing your 401(k) contribution by 1.5%, slightly improving your lifestyle with the remaining 1.5%, and paying no additional taxes on the portion going to pre-tax retirement accounts.

Always prioritize capturing the full employer match before anything else. This is free money with immediate guaranteed returns you’ll never find elsewhere. After that, eliminate high-interest debt, build your emergency fund, then scale up retirement investing as aggressively as your budget allows.

Step 7: Protect Your Financial Plan with Insurance

Building wealth takes years or decades. Adequate insurance ensures that unexpected events don’t destroy everything you’ve worked to create. Think of insurance as the foundation protecting your entire financial house.

Essential Insurance Types

Health insurance prevents medical emergencies from causing financial devastation. Without it, a single hospitalization can result in six-figure bills leading to bankruptcy. Even with insurance, understand your plan’s deductibles, out-of-pocket maximums, and network requirements. If your employer offers health insurance, take it. If not, explore marketplace plans through Healthcare.gov. The penalty for going uninsured isn’t just financial risk—it’s gambling with both your health and finances.

Auto insurance is legally required in most states, but the minimum liability coverage often isn’t enough. If you cause an accident injuring someone seriously, minimum coverage may not cover damages, leaving you personally liable. Consider liability coverage of at least $250,000/$500,000 (per person/per accident). Collision and comprehensive coverage protect your vehicle, though you might skip these for older cars worth less than $3,000-4,000.

Renters insurance is inexpensive—often $15-30 monthly—yet most renters skip it. This coverage protects your personal belongings (furniture, electronics, clothing) from theft, fire, or water damage. It also provides liability protection if someone is injured in your rental. Your landlord’s insurance covers the building, not your possessions.

Homeowners insurance is required by mortgage lenders and protects your largest asset. Coverage includes the dwelling structure, personal belongings, liability, and additional living expenses if your home becomes uninhabitable. Don’t underinsure—replacement cost should reflect current building costs, which may exceed your home’s market value.

Life insurance becomes essential when others depend on your income—a spouse, children, or aging parents you support. Term life insurance is simple and affordable for most people. A $500,000 20-year term policy for a healthy 30-year-old might cost $25-40 monthly. The coverage replaces your income if you die, allowing dependents to maintain their lifestyle, pay off debts, and cover future expenses like college. If no one relies on your income, you probably don’t need life insurance yet.

Disability insurance protects your income if illness or injury prevents you from working. Given that you’re more likely to become disabled than die during working years, this coverage is crucial yet often overlooked. Many employers offer group disability insurance—review your benefits and consider supplemental coverage if the group policy only replaces 50-60% of income.

How Much Coverage Do You Need?

Life insurance coverage typically follows the rule of 10-12 times your annual income. Someone earning $50,000 should carry $500,000-600,000 in coverage. This ensures your family can invest the payout and live off investment returns while preserving the principal. Alternatively, calculate specific needs: remaining mortgage balance, college funds for children, debt to pay off, and years of income replacement.

Understanding deductibles and premiums is crucial for balancing cost with protection. Deductibles are what you pay out-of-pocket before insurance kicks in. Higher deductibles mean lower monthly premiums. A good strategy is setting deductibles at the top end of what your emergency fund could cover—perhaps $1,000-2,500. This lowers premiums significantly while keeping coverage for truly catastrophic events.

Balance cost with adequate protection by covering catastrophic risks comprehensively while accepting more risk on smaller losses. It’s better to have high-deductible coverage for big disasters than low-deductible coverage with such low limits that it won’t help when you really need it.

Where to Find Affordable Insurance

Employer-sponsored insurance is usually your best option for health, life, and disability coverage. Employers negotiate group rates and often subsidize premiums. Review your employer benefits thoroughly during open enrollment.

For health insurance without employer coverage, check Healthcare.gov for marketplace plans. Depending on income, you may qualify for subsidies reducing premiums and out-of-pocket costs.

Independent insurance agents can shop multiple companies for auto, home, and life insurance, potentially saving hundreds annually. Unlike captive agents who represent one company, independent agents compare options across insurers.

Look for discount opportunities: bundling home and auto insurance with one company often saves 15-25%, maintaining good credit improves rates, taking defensive driving courses can reduce auto premiums, installing home security systems lowers homeowners premiums, and increasing deductibles significantly reduces premiums if you have emergency savings to cover them.

Never let insurance coverage lapse trying to save money. Gaps in coverage can lead to higher rates when you reapply and leave you exposed to potentially devastating financial losses. Insurance is not optional—it’s a fundamental component of financial security.

Step 8: Review and Adjust Your Plan Regularly

Creating a personal finance plan isn’t a one-time event—it’s an ongoing process requiring regular attention and adjustment. Life changes, goals evolve, and your plan must adapt accordingly.

Monthly Financial Check-Ins

Set aside 30-45 minutes monthly for a financial review. This consistent habit keeps you aware, on track, and able to course-correct quickly.

Review your budget versus actual spending. Did you stay within limits? Which categories went over or under? Don’t beat yourself up over occasional overspending—look for patterns. If dining out consistently exceeds budget, either allocate more money to that category or develop strategies to reduce restaurant spending.

Track progress toward your financial goals. Update your net worth spreadsheet. Check account balances. Calculate debt payoff progress. Update your goal tracking charts. Seeing concrete progress—even slow progress—maintains motivation and momentum.

Adjust for life changes as they occur. Got a raise? Increase retirement contributions and savings. New recurring expense? Build it into your budget. Unexpected windfall? Decide intentionally how to allocate it rather than letting lifestyle inflation absorb it. The key is being proactive rather than reactive.

Celebrate wins and learn from setbacks without judgment. Paid off a credit card? That’s worth celebrating! Overspent this month? Examine why, adjust your strategy, and move forward. Financial progress isn’t linear—expect ups and downs while maintaining overall forward momentum.

Quarterly Financial Reviews

Every three months, conduct a more comprehensive financial review beyond monthly tracking.

Rebalancing your investment portfolio means returning to your target asset allocation. If stocks have performed well, they might grow from your target 80% to 85% of your portfolio. Rebalancing means selling some stocks and buying bonds to return to 80/20. This enforces the wise discipline of “sell high, buy low.” Most people rebalance annually or semi-annually, though quarterly works if allocations have drifted significantly.

Check your credit score and report quarterly to monitor for identity theft, score changes, and accuracy. Many credit cards now provide free credit score monitoring. Seeing your score improve as you pay down debt and manage credit responsibly provides tangible evidence of your financial progress.

Evaluate insurance coverage to ensure it still meets your needs. Had a baby? You need more life insurance. Bought expensive electronics? Your renters insurance might need increased coverage. Paid off your car? Consider dropping collision/comprehensive coverage on an older vehicle.

Assess emergency fund adequacy, especially if your expenses have changed. Got a new job with better stability? Three months might suffice. Started freelancing? Increase to six months. Quarterly reviews catch these shifts before they become problematic.

Annual Financial Planning

Once yearly, conduct a comprehensive financial review and planning session. Many people do this in December or January, but any consistent annual timing works.

Set new goals for the year aligned with your values and overall plan. These might be financial goals (increase retirement contributions by 2%, save $5,000 for vacation, pay off $10,000 in student loans) or life goals with financial implications (change careers, start a family, move to a new city).

Optimize your tax situation by reviewing deductions, retirement contributions, and tax-advantaged account usage. Consider meeting with a tax professional if you have questions. Tax planning is legal and smart—you should take every deduction and credit you’re entitled to.

Increase retirement contributions annually, especially if you received raises. A 3% cost-of-living increase in salary provides an excellent opportunity to increase your 401(k) contribution by 1%, improving your future while barely impacting your present lifestyle.

Review all financial accounts and clean up what you don’t need. Close old credit cards you’re not using (keep your oldest cards open for credit history), consolidate old 401(k)s from previous employers into an IRA, close bank accounts with fees, and simplify where possible. Financial complexity creates friction—the simpler your system, the easier to maintain.

Consider working with a fee-only financial planner for a one-time comprehensive review. This is especially valuable during major life transitions (marriage, home purchase, career change, inheritance) or when approaching retirement.

Common Mistakes to Avoid When Creating Your Financial Plan

Learning from others’ mistakes is cheaper and less painful than learning from your own. Avoid these common pitfalls that derail many beginners’ financial plans.

Mistake #1: Not Starting Because It Feels Overwhelming

Analysis paralysis keeps many people from ever beginning their financial journey. They research endlessly, seeking the “perfect” plan, optimal investment strategy, or ideal moment to start. Meanwhile, time—their most valuable asset—slips away.

The danger of analysis paralysis is that perfect never comes. There’s always more to learn, better strategies to discover, more optimal timing to wait for. Waiting to start until you understand everything perfectly means never starting at all.

Starting imperfectly is infinitely better than not starting. Open a high-yield savings account even if you’re not sure it’s the absolute best rate available. Start contributing to your 401(k) even if you haven’t optimized your asset allocation yet. Create a simple budget even if it’s not the mathematically ideal budgeting system.

Break down big goals into small, immediate actions. “Get my finances in order” is overwhelming. “Calculate my net worth today” is manageable. “Open a Roth IRA” is actionable. “Transfer $100 to savings this week” you can do right now. Small actions build momentum, momentum builds confidence, and confidence enables bigger actions.

Give yourself permission to be a beginner. You don’t need to understand every financial concept before taking basic steps. Learn as you go, adjust as you grow, and trust that imperfect action beats perfect inaction every time.

Mistake #2: Forgetting to Budget for Irregular Expenses

Most people budget monthly income and expenses without accounting for irregular costs that occur less frequently. Then when annual insurance premiums, holiday shopping, or vehicle registration fees arrive, they’re surprised and forced to go into debt or raid emergency funds.

Annual expenses still need monthly planning. Car insurance costs $1,200 annually? Set aside $100 monthly. Amazon Prime is $140 yearly? Budget $12 monthly. Holiday shopping costs $1,000? Save $85 monthly starting in January. By budgeting monthly for irregular expenses, the money is available when needed.

Seasonal costs like holidays, back-to-school shopping, and summer vacations are predictable yet frequently overlooked in monthly budgets. Create a “sinking fund” system—separate savings accounts or budget categories where you accumulate money for known future expenses.

Vehicle maintenance and repairs are guaranteed, though timing is unpredictable. Budget $100-150 monthly for eventual repairs, oil changes, tire replacements, and registration fees. Newer vehicles might need less, older vehicles more, but something will need attention eventually.

Medical expenses including deductibles, copays, prescriptions, and dental/vision care often surprise people. Review last year’s medical spending and budget monthly toward next year’s likely costs. If you have a health savings account (HSA) with a high-deductible health plan, maximize contributions for triple tax benefits.

The key is reviewing your past 12 months of spending to identify all irregular expenses, calculating the annual total for each category, dividing by 12, and including that monthly amount in your budget. This simple step eliminates most “unexpected” expenses.

Mistake #3: Not Automating Your Finances

Relying on willpower and memory to manage your finances guarantees eventual failure. Willpower is a limited resource that depletes throughout the day. Automation removes the need for willpower, making good financial behavior effortless.

Benefits of automatic bill pay include never missing due dates, avoiding late fees and credit score damage, and eliminating the mental energy of remembering payment dates. Set up automatic payments for all fixed recurring expenses: rent or mortgage, utilities, insurance, loan payments, and subscriptions.

Auto-transfers to savings and investment accounts ensure consistent progress toward goals. Schedule transfers immediately after payday when your checking balance is highest. Transfer to emergency savings, Roth IRA, taxable investment accounts, or goal-specific savings accounts. The money moves before you have a chance to spend it.

Automation reduces decision fatigue—the exhaustion from making constant choices. Every decision whether to transfer money to savings, pay extra on debt, or spend on something else depletes mental energy. Automation makes these decisions once during setup, then executes automatically forever.

The “pay yourself first” philosophy means treating savings and investments as non-negotiable expenses paid before anything else. When your paycheck deposits, automatic transfers immediately move money to your financial goals. You then live on whatever remains. This ensures your future self always gets funded, even when your present self wants to overspend.

Set up automation thoughtfully—ensure adequate checking account buffers to avoid overdrafts, monitor accounts initially to confirm transfers execute correctly, and schedule transfers to align with your pay schedule. Once established, automation runs quietly in the background, consistently building your financial future.

Mistake #4: Comparing Your Journey to Others

Social media presents a distorted reality of others’ financial lives. You see friends’ vacation photos, new car purchases, restaurant dinners, and home renovations without seeing the credit card debt, financial stress, or wealthy parents funding it all. Comparing your behind-the-scenes reality to others’ highlight reels breeds dissatisfaction and poor financial decisions.

Everyone’s financial situation is completely unique. Different starting points, income levels, expenses, family obligations, health situations, and goals mean someone else’s perfect plan might be wrong for you. Your friend driving a luxury car might be drowning in debt while you’re building real wealth living modestly.

Focus exclusively on your own progress rather than comparing to others. Are you better off financially than you were six months ago? A year ago? That’s what matters. Celebrate improving your own situation regardless of what others appear to be doing.

The danger of lifestyle inflation is especially acute when comparing yourself to others. As your income increases, the temptation to upgrade your lifestyle to match peers can consume every raise. Your friend bought a bigger house, so you feel your home is inadequate. Coworkers lease new cars every three years, so your paid-off vehicle feels embarrassing. Resist these comparisons.

True wealth is built by keeping expenses stable as income rises, directing the difference toward savings and investments. The millionaire next door often drives a decade-old car, lives in a modest home, and spends less than they earn—not because they have to, but because they choose to. That’s how ordinary income becomes extraordinary wealth.

Mistake #5: Not Building Fun Into Your Budget

Perhaps the most common reason financial plans fail is making them too restrictive. Budgets built on deprivation and denial work briefly before people rebel and abandon them entirely. The pendulum swings from extreme restriction to excessive spending, making no real progress.

Sustainable financial plans balance future security with present enjoyment. Yes, you’re saving for retirement in 30 years, but you’re also living today. Your budget must include guilt-free spending money for things that bring joy, even if they’re not strictly “needs.”

Allocate “fun money” or discretionary spending based on your situation. If you’re in aggressive debt payoff mode, maybe it’s just $50 monthly. If you’re in a stable phase, perhaps 10-15% of income goes to entertainment, hobbies, dining out, and spontaneous purchases. The exact amount matters less than having some amount designated for enjoyment.

Avoiding burnout and restriction mindset is crucial for long-term success. Financial restriction triggers the same psychological response as extreme dieting—initial compliance followed by rebellion and bingeing. Build treats and flexibility into your plan from the beginning rather than swinging between extremes.

Balance present enjoyment with future security by asking whether spending aligns with your values. Maybe you don’t care about fancy cars but love travel—spend less on transportation, more on experiences. Perhaps you’re a homebody who loves entertaining—invest in your home, skip expensive outings. Spend meaningfully on what truly matters to you while cutting ruthlessly on what doesn’t.

Remember that personal finance is personal. Your plan should reflect your unique values, goals, and priorities—not someone else’s definition of “should.” Build a plan you can actually live with, not just survive under temporarily.

Tools and Resources for Managing Your Personal Finances

Successful personal finance management is much easier with the right tools. Modern technology provides powerful resources, many completely free, that simplify tracking, planning, and growing your wealth.

Budgeting Apps and Software

Mint is the most popular free budget tracking app. It connects to your bank accounts, credit cards, and loans to automatically categorize transactions and track spending across categories. Mint provides budget alerts when you’re approaching category limits, credit score monitoring, and bill payment reminders. The interface is user-friendly and the price is right—completely free, supported by targeted financial product offers.

YNAB (You Need A Budget) costs $14.99 monthly or $99 annually but offers a powerful zero-based budgeting system. YNAB’s philosophy is giving every dollar a job, planning ahead for expenses, and adjusting your plan as life happens. The app includes excellent educational resources, supportive community forums, and a proven methodology. Many users report that YNAB pays for itself many times over through better money management.

Personal Capital is technically a wealth management platform, but its free tools are excellent for tracking net worth, analyzing investments, and planning retirement. Personal Capital shines in the investment tracking and fee analysis features, showing exactly how much you’re paying in investment fees and how they impact long-term wealth. Like Mint, it’s free with optional paid wealth management services.

EveryDollar by Ramsey Solutions offers simple budgeting aligned with Dave Ramsey’s financial principles. The free version provides basic budgeting functionality, while the paid version ($79.99 annually) connects to your bank accounts for automatic transaction import. The app is straightforward and perfect for beginners who want simplicity without overwhelming features.

Each tool has pros and cons. Mint is free and automated but can be glitchy with bank connections. YNAB requires a subscription but provides superior methodology and support. Personal Capital excels at investment tracking but isn’t primarily a budget tool. EveryDollar is simple but the manual transaction entry in the free version is tedious. Try a few options to find what works for your needs and preferences.

Investment Platforms for Beginners

Vanguard is renowned for low-cost index funds and investor-focused philosophy. Vanguard is structured as a mutual company owned by its funds, which are owned by investors—meaning investors own Vanguard. This unique structure aligns incentives toward keeping costs low. Many Vanguard index funds charge expense ratios under 0.10%, and some are as low as 0.03%. Minimum initial investments vary but many funds require $1,000-3,000 to start.

Fidelity offers zero-expense-ratio index funds and excellent customer service. Fidelity’s ZERO funds (FZROX, FZILX, etc.) charge literally 0.00% in expenses—the lowest possible. Fidelity also provides extensive research tools, retirement planning calculators, and no minimum investment requirements for most accounts. The platform works well for beginners and sophisticated investors alike.

Betterment is a leading robo-advisor that builds and manages diversified portfolios automatically. You answer questions about goals, timeline, and risk tolerance, then Betterment creates an appropriate portfolio of low-cost ETFs. The platform automatically rebalances, harvests tax losses, and adjusts allocation as you near goals. Management fees are 0.25% annually (plus underlying ETF expenses), with no minimum balance required.

Acorns focuses on micro-investing by rounding up everyday purchases to the nearest dollar and investing the spare change. Buy coffee for $4.50, Acorns rounds to $5.00 and invests $0.50. This frictionless approach helps beginners start investing without feeling the impact. Accounts cost $3-12 monthly depending on tier, making it less cost-effective for small balances but useful for building the investing habit.

M1 Finance offers free automated investing combining robo-advisor convenience with DIY control. You create a “pie” of stocks and ETFs in your desired allocation, set up automatic deposits, and M1 automatically invests to maintain your target allocation. There are no trading commissions or management fees, making it excellent for cost-conscious investors who want some customization.

For most beginners, starting with a robo-advisor like Betterment or using low-cost index funds at Fidelity or Vanguard is the best approach. As you learn more and feel more comfortable, you can always transition to more hands-on management if desired.

Educational Resources

Books provide foundational financial knowledge. “The Total Money Makeover” by Dave Ramsey offers a straightforward debt-elimination and wealth-building plan perfect for beginners drowning in debt. “Your Money or Your Life” by Vicki Robin transforms how you think about money and its relationship to your time and life energy. “The Simple Path to Wealth” by JL Collins provides clear, no-nonsense guidance on investing and building wealth. “I Will Teach You to Be Rich” by Ramit Sethi offers a practical 6-week program for financial automation and optimization.

Podcasts fit financial education into commute time or workouts. “The Dave Ramsey Show” features real caller situations and debt-free screams celebrating financial wins. “ChooseFI” focuses on financial independence and optimizing life for fulfillment rather than maximum income. “The Money Guy Show” provides practical advice and deep dives into financial topics. “Afford Anything” by Paula Pant explores the trade-offs in spending, investing, and life design.

YouTube channels offer visual learning and specific how-to guidance. Graham Stephan covers real estate investing, credit card optimization, and wealth building. The Financial Diet provides approachable advice for millennials and Gen Z. Two Cents by PBS explains economic and financial concepts clearly. Andrei Jikh focuses on investing, credit strategies, and financial independence.

Free courses from reputable sources include Khan Academy’s personal finance sections, Coursera’s financial planning courses from universities, and the FDIC’s Money Smart program. These provide structured learning at no cost.

The key to financial education is starting wherever you are and consuming content consistently. Even 15 minutes daily of financial podcasts or reading compounds into substantial knowledge over months and years.

Finding Professional Help

Most beginners can successfully manage their finances without professional help using the resources mentioned above. However, certain situations warrant working with a financial advisor.

Consider a financial advisor when you have complex situations like inheritance or large windfalls, business ownership requiring tax optimization, complicated tax situations, significant assets requiring sophisticated management, or major life transitions like divorce or retirement. Also consider professional help if you’ve built substantial wealth and want comprehensive planning, or if you simply want peace of mind from professional guidance despite being capable of DIY management.

Fee-only advisors charge for their time and expertise but don’t earn commissions on products they recommend. This structure aligns incentives—they succeed when you succeed, not when they sell you something. Fee-only advisors might charge hourly rates ($150-400), flat fees for specific services ($1,000-3,000 for a financial plan), or percentage of assets managed (typically 0.5-1.5% annually).

Commission-based advisors earn money by selling financial products—insurance, mutual funds, annuities. This creates potential conflicts of interest, as they might recommend products with higher commissions rather than what’s truly best for you. Some advisors are “fee-based” (not fee-only), meaning they charge fees and earn commissions—still a potential conflict.

The Certified Financial Planner (CFP) designation indicates rigorous education, examination, experience, and ethics requirements. A CFP has studied comprehensive financial planning including investments, taxes, retirement, estate planning, and insurance. While certification doesn’t guarantee quality, it does demonstrate commitment to the profession and adherence to ethical standards.

Free financial counseling resources exist through nonprofit organizations. The National Foundation for Credit Counseling (NFCC) provides free or low-cost counseling for budgeting and debt management. Many employers offer free financial wellness programs through their benefits. Some community organizations and libraries offer free financial education workshops.

If you do work with an advisor, understand exactly how they’re compensated, ensure they’re a fiduciary (legally required to act in your best interest), verify credentials, and ask for references. A good advisor educates you, empowers you, and makes you more confident about your finances—not more dependent on them.

| App | Cost | Best For | Key Features | Bank Connection |

|---|---|---|---|---|

| Mint | Free | Budget tracking & automation | Auto-categorization, budget alerts, credit monitoring | Yes – automatic |

| YNAB | $99/year | Zero-based budgeting enthusiasts | Goal-oriented methodology, education, support | Yes – automatic (paid) |

| Personal Capital | Free | Investment tracking & net worth | Investment analysis, fee analyzer, retirement planner | Yes – automatic |

| EveryDollar | Free / $80/year | Simple budget beginners | Easy interface, Ramsey methodology, simplicity | Premium only |

FAQs

How much money do I need to start a personal finance plan?

You don’t need any money to start creating a personal finance plan. The planning process begins with assessing your currentsituation, setting goals, and creating a budget—all of which cost nothing. Once you have a plan in place, you can start withas little as $10-25 per paycheck toward your emergency fund or debt payoff. The key is to start where you are and graduallybuild from there.

How long does it take to see results from a financial plan?

Most beginners see initial results within 30-60 days, such as better awareness of spending habits and a small emergency fund. Significant results like paying off debt or building substantial savings typically take 6-12 months. Long-term goals like retirement planning show results over decades. The important thing is that you’re making progress, even if it feels slow initially.

Should I pay off debt or save money first?

For beginners, the recommended approach is to save a small starter emergency fund ($500-1,000) first, then focus on payingoff high-interest debt (credit cards above 15% APR), then build your full emergency fund (3-6 months of expenses). Thisbalanced approach prevents you from going further into debt when emergencies arise while still tackling expensive debt.

Do I need a financial advisor to create a personal finance plan?

Most beginners can successfully create and manage their own financial plan using free resources, apps, and educationalmaterials. A financial advisor becomes valuable when you have complex situations (inheritance, business ownership,complex tax situations) or significant assets to manage. Start with self-education and DIY planning, and considerprofessional help as your financial situation becomes more complex.

What if I have irregular income as a freelancer or gig worker?

Creating a personal finance plan with irregular income requires a few adjustments: budget based on your lowest monthlyincome from the past year, build a larger emergency fund (6-12 months), separate business and personal finances, set asidemoney for taxes quarterly, and create a “profit first” system where you pay yourself a consistent salary. The principlesremain the same—you just need more flexibility and buffer.

How often should I update my personal finance plan?

Review your budget monthly, conduct a more thorough financial review quarterly, and do a comprehensive annual reviewwhere you reassess goals, update net worth, and adjust your plan for life changes. Additionally, update your plan wheneveryou experience major life events (job change, marriage, having children, buying a home).

Is it too late to start if I’m in my 30s, 40s, or older?

It’s never too late to start managing your finances better. While starting younger gives you more time for compound interest to work, people who start in their 30s, 40s, or even 50s can still build substantial wealth and achieve financial security. The best time to start was yesterday; the second-best time is today. Focus on maximizing the time you have left rather than regretting time lost.

Conclusion