Turn Your Dreams into Goals: How to Plan and Reach Your Savings Targets

We all have dreams. Maybe you’re picturing yourself on a beach vacation, driving a new car, or finally moving into your own home. These visions feel wonderful—until you check your bank account and wonder if they’ll ever become reality.

Here’s the truth: dreams without a plan are just wishes. But when you transform those dreams into concrete savings goals with a clear roadmap, something magical happens. Suddenly, that beach vacation isn’t just a fantasy—it’s a destination with an arrival date.

If you’ve ever felt overwhelmed by saving money or unsure where to start, you’re not alone. According to a 2023 Bankrate survey, nearly 57% of Americans can’t cover a $1,000 emergency expense from savings. The problem isn’t that people don’t want to save; it’s that they don’t have a systematic approach to turn their financial dreams into achievable goals.

This comprehensive guide will walk you through every step of transforming your dreams into tangible savings targets—and actually reaching them. Whether you’re saving for a vacation, an emergency fund, a down payment, or retirement, these proven strategies will help you get there.

Understanding the Difference: Dreams vs. Goals

Before we dive into the planning process, let’s clarify an important distinction.

Dreams are vague and emotional. “I want to travel the world someday” or “I wish I could retire early” are dreams. They inspire us, but they lack specificity and actionable steps.

Goals are specific, measurable, and time-bound. “I will save $3,000 for a two-week European vacation by December 2026” is a goal. It has a clear target, a defined amount, and a deadline.

The transformation from dream to goal happens when you add three critical elements:

- Specificity: Exactly what do you want?

- Quantification: How much will it cost?

- Timeline: When do you want to achieve it?

Think of your dream as the destination and your goal as the GPS coordinates that will actually get you there.

Step 1: Identify and Prioritize Your Financial Dreams

Start by brainstorming all the things you want to save for. Don’t filter yourself yet—just write everything down. Your list might include:

- Emergency fund (3-6 months of expenses)

- Vacation or travel experiences

- Down payment on a home

- New or used car

- Wedding expenses

- Starting a business

- Children’s education

- Home renovations

- Retirement fund

- Paying off debt

Once you have your list, categorize your dreams by timeline:

Short-term (0-2 years): Emergency fund, vacation, minor purchases Medium-term (2-5 years): Car, wedding, home down payment Long-term (5+ years): Retirement, children’s education, major life changes

Next, prioritize ruthlessly. You can’t save for everything at once, especially when you’re just starting. Ask yourself:

- Which goal would have the biggest positive impact on my life right now?

- Which goal would provide the most financial security?

- Which goal is most time-sensitive?

Pro tip: Most financial experts recommend building a basic emergency fund ($1,000-$2,000) before tackling other goals. This prevents you from derailing your savings plan when unexpected expenses arise.

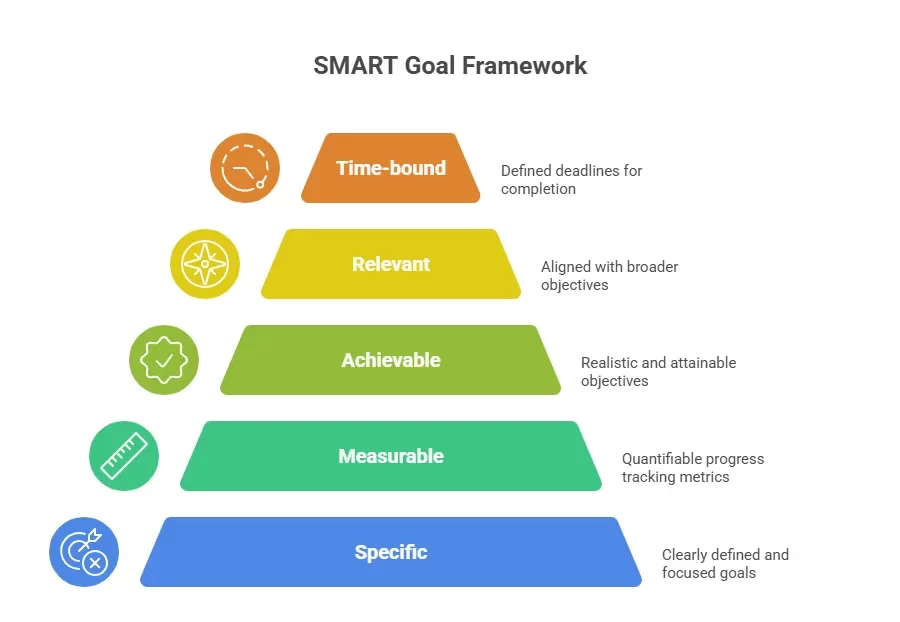

Step 2: Turn Dreams into SMART Goals

Now it’s time to apply the SMART framework to transform your prioritized dreams into actionable goals. SMART stands for:

Specific: Define exactly what you’re saving for Measurable: Attach a dollar amount Achievable: Ensure it’s realistic given your income Relevant: Confirm it aligns with your values Time-bound: Set a clear deadline

Let’s look at examples:

Vague dream: “I want to save money for emergencies” SMART goal: “I will save $5,000 in an emergency fund within 12 months by setting aside $420 per month”

Vague dream: “I’d love to take a nice vacation” SMART goal: “I will save $2,400 for a one-week Hawaii vacation in 18 months by saving $135 per month”

Notice how the SMART version immediately tells you what you need to do each month to reach your target. This clarity eliminates guesswork and builds confidence.

Step 3: Calculate the Real Cost

One of the biggest mistakes people make is underestimating how much their goals will actually cost. This leads to frustration when you reach your “target” but can’t afford what you wanted.

For each goal, research the true cost:

For a vacation: Include flights, accommodation, food, activities, travel insurance, and spending money. Add a 10-15% buffer for unexpected costs.

For a home down payment: Consider not just the down payment percentage (typically 3-20% of the home price) but also closing costs, moving expenses, immediate repairs, and furniture.

For an emergency fund: Calculate 3-6 months of your actual expenses, not your income. Include rent/mortgage, utilities, food, insurance, minimum debt payments, and transportation.

For retirement: Use online retirement calculators that factor in your current age, desired retirement age, expected lifestyle, and inflation.

Don’t forget to account for inflation on long-term goals. A college education or home that costs $200,000 today might cost $260,000 in 10 years with 3% annual inflation.

Step 4: Assess Your Current Financial Situation

You can’t plan a route without knowing your starting point. Take an honest look at your finances:

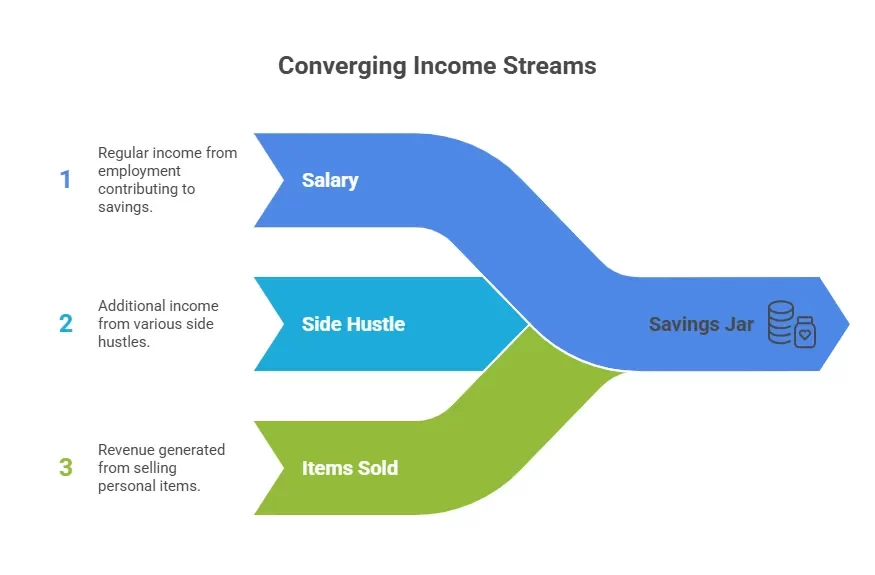

Calculate Your Monthly Income

Include all sources: salary (after taxes), side hustles, freelance work, investment income, and any other regular income streams.

Track Your Current Expenses

For one month, record every single expense. Use apps like Mint, YNAB (You Need A Budget), or PocketGuard, or simply use a spreadsheet. Categorize expenses as:

- Fixed necessities: Rent, insurance, loan payments

- Variable necessities: Groceries, utilities, gas

- Discretionary: Entertainment, dining out, subscriptions

Calculate Your Savings Capacity

Subtract your total expenses from your income. The remainder is your potential savings amount. If this number is zero or negative, don’t panic—we’ll address that in the next step.

Review Your Debt

List all debts with interest rates. High-interest debt (credit cards above 15-20%) should typically be paid off before aggressive saving, as the interest costs more than you’d earn in savings.

Step 5: Create Your Savings Roadmap

Now comes the exciting part—building your personalized savings plan.

Calculate Monthly Contributions

For each goal, divide the total amount needed by the number of months until your deadline:

Monthly savings needed = Total goal amount ÷ Number of months

Example: $6,000 emergency fund in 18 months = $333/month

Use the Multiple Savings Buckets Strategy

Don’t mix all your goals into one account. Instead, create separate “buckets” (savings accounts or sub-accounts) for each goal:

- Emergency Fund Savings

- Vacation Fund

- House Down Payment Fund

- Car Replacement Fund

Many banks offer free savings accounts with no minimum balances. Some excellent options include Marcus by Goldman Sachs, Ally Bank, and Capital One 360, which offer higher interest rates than traditional banks and allow multiple savings goals.

Label each account clearly. When you see your “Hawaii Vacation Fund” growing, it’s more motivating than watching a generic savings account increase.

Automate Everything

This is the single most powerful savings strategy: automate your contributions immediately after payday.

Set up automatic transfers from your checking account to your various savings accounts the day after your paycheck deposits. This “pay yourself first” approach ensures you save before you have a chance to spend.

According to research from the National Bureau of Economic Research, people who automate their savings save significantly more than those who manually transfer money—because automation removes willpower from the equation.

Build in Flexibility

Life happens. Create a buffer in your plan:

- Add an extra 10% to your timeline (if saving for 12 months, plan for 13-14)

- Include a “variable contributions” line item for bonuses or windfalls

- Review and adjust quarterly—if your income increases, boost contributions

Step 6: Find Extra Money to Save

If your current income barely covers expenses, you’ll need to either increase income or decrease expenses (or both).

Cut Expenses Strategically

Don’t start by eliminating everything you enjoy—that’s unsustainable. Instead, focus on these high-impact areas:

Subscriptions and memberships: Cancel unused gym memberships, streaming services you rarely watch, or magazine subscriptions. Potential savings: $50-150/month

Food costs: Meal plan, cook at home more often, and pack lunches. This doesn’t mean eating ramen every day—just being more intentional. Potential savings: $200-400/month

Shop your insurance: Get quotes for car and home insurance annually. Switching carriers can save hundreds. Potential savings: $50-200/month

Negotiate bills: Call providers for internet, phone, and cable to request better rates. Say you’re comparing competitors. Potential savings: $40-100/month

Reduce energy costs: Small changes like LED bulbs, programmable thermostats, and unplugging devices save money. Potential savings: $30-80/month

Increase Your Income

Sometimes cutting expenses isn’t enough. Consider:

- Side hustles: Freelancing, tutoring, pet-sitting, ride-sharing, or selling items online

- Ask for a raise: Research market rates for your position and present your case professionally

- Develop new skills: Take online courses to qualify for higher-paying positions

- Sell unused items: That closet full of things you don’t use could be $500-2,000 in savings

Step 7: Track Progress and Stay Motivated

The journey to your savings goal can take months or years. Maintaining motivation is crucial.

Visual Tracking Methods

Choose a tracking method that resonates with you:

- Savings thermometer: Draw or print a thermometer and color it in as you progress

- Milestone celebrations: Celebrate every 25% of your goal reached with a small, inexpensive treat

- Progress photos: Take monthly screenshots of your account balances

- Countdown calendar: Cross off weeks or months as you get closer

Regular Check-ins

Schedule monthly “money dates” with yourself (or your partner if you share finances):

- Review all account balances

- Celebrate progress, no matter how small

- Identify any obstacles or challenges

- Adjust the plan if circumstances changed

- Recommit to your “why”

Protect Your Savings

The temptation to dip into savings for non-emergencies will arise. Protect yourself:

- Keep savings in a separate bank from your checking account (adds friction to withdrawals)

- Remove debit cards associated with savings accounts

- Create a “24-hour rule” before any unplanned withdrawal

- Have an accountability partner who knows your goals

Overcome Common Obstacles

Obstacle: “I had an unexpected expense and had to use my savings” Solution: This is why emergency funds come first. Rebuild it immediately.

Obstacle: “I’m not seeing progress fast enough” Solution: Remember that $50/month is $600/year. Small amounts compound over time.

Obstacle: “I got discouraged and stopped tracking” Solution: Don’t let perfection be the enemy of progress. Resume immediately—every day is a fresh start.

Step 8: Optimize Your Savings with Smart Strategies

Once you’re consistently saving, maximize your efforts with these advanced strategies:

Choose the Right Savings Vehicles

High-yield savings accounts: For short and medium-term goals. Currently offering 4-5% annual interest (rates fluctuate). FDIC insured up to $250,000.

Certificates of Deposit (CDs): For money you won’t need for 6 months to 5 years. Often higher rates than savings accounts but locks your money for a term.

Money Market Accounts: Combines checking and savings features with higher interest than traditional savings.

Investment accounts: For long-term goals (5+ years), consider index funds or target-date retirement funds. Higher potential returns but also higher risk and volatility.

529 Plans: Specifically for education savings, offering tax advantages.

Retirement accounts (401k, IRA): Tax-advantaged accounts for retirement savings. Many employers match contributions—free money you shouldn’t leave on the table.

Supercharge with Windfalls

Commit to saving at least 50% of any unexpected money:

- Tax refunds

- Work bonuses

- Birthday or holiday money

- Inheritance

- Raises (save the difference between old and new pay)

This accelerates your timeline without impacting your regular budget.

Use the Power of Compound Interest

Even modest interest rates make a difference over time. $10,000 in a 4% high-yield savings account grows to $10,816 in two years—that’s $816 in free money just for letting it sit there.

For long-term goals, compound interest becomes even more powerful. $5,000 invested annually at 7% average return grows to over $505,000 in 30 years.

Real-Life Success Stories

Sarah’s Emergency Fund Journey: Sarah, a 28-year-old teacher, felt anxious about financial instability. She committed to saving $3,000 in one year. By cutting her $150/month dining-out budget in half and picking up summer tutoring jobs, she saved $275/month. After 11 months, she reached her goal—and felt empowered to tackle her next goal: a down payment.

The Martinez Family Vacation Fund: The Martinez family dreamed of taking their three kids to Disney World but thought it was impossible on one income. They set a goal of $4,500 in two years. By saving birthday money, selling unused items, and allocating $150/month from their budget, they took their dream vacation and created memories that last a lifetime.

James’s Career Change Fund: James wanted to leave his corporate job and start a business but needed a safety net. He calculated he needed $15,000 for six months of expenses. Over 18 months, he automated $500/month savings, took on weekend freelance projects, and saved every bonus. He launched his business with confidence, knowing he had a financial cushion.

These stories prove that ordinary people with clear goals and consistent action can achieve extraordinary results.

Your Action Plan: Get Started Today

You don’t need to wait until Monday or next month. Here’s what to do right now:

Today (15 minutes):

- Choose your top priority savings goal

- Research the realistic cost

- Set your deadline

- Calculate monthly savings needed

This Week (1 hour):

- Open a separate high-yield savings account

- Set up automatic transfers

- Track your expenses for 7 days to find potential cuts

- Create a visual tracker

This Month (ongoing):

- Implement one expense reduction strategy

- Transfer your first savings amount

- Set a calendar reminder for monthly check-ins

- Tell one supportive person about your goal for accountability

Conclusion: Your Dreams Are Closer Than You Think

Transforming dreams into achievable savings goals isn’t about deprivation or making your life less enjoyable. It’s about getting intentional with your money so it serves your real priorities instead of disappearing into forgotten purchases.

The distance between where you are now and where you want to be isn’t as far as it seems. It’s bridged by small, consistent actions—automatic transfers, thoughtful choices, and maintaining your focus on what truly matters to you.

Your dream vacation, secure emergency fund, or comfortable retirement isn’t just possible—it’s probable when you follow a systematic plan. Millions of people just like you have transformed their financial futures by taking the exact steps outlined in this guide.

The question isn’t whether you can reach your savings targets. The question is: when will you start?

Your future self is waiting on the other side of that decision. Make today the day you turn your dreams into goals—and your goals into reality