How to Adjust Budgets Through Life Changes (Marriage, Job Loss, Children)

Life rarely follows a straight path. One moment you’re cruising along with a comfortable financial routine, and the next, you’re getting married, welcoming a baby, or navigating an unexpected job loss. These pivotal moments don’t just reshape your daily life—they fundamentally transform your financial landscape.

Learning how to adjust budgets through life changes (marriage, job loss, children) is one of the most valuable skills you can develop. Whether you’re merging finances with a spouse, stretching dollars during unemployment, or preparing for the costs of raising a child, your budget needs to evolve alongside your circumstances. This comprehensive guide will walk you through proven strategies to keep your finances stable and thriving, no matter what life throws your way.

Understanding Budget Adjustments: The Basics

Before diving into specific life scenarios, let’s establish what budget adjustment actually means and why it’s crucial for your financial health.

What Does Adjusting Your Budget Mean?

Adjusting your budget means reviewing and modifying your income allocation and spending plan to reflect changes in your financial situation, responsibilities, or goals. It’s not about starting from scratch every time something changes—it’s about being flexible and responsive to your evolving needs.

Think of your budget as a living document rather than a rigid rulebook. Just as you wouldn’t wear the same clothes in every season, your budget shouldn’t remain static when your life circumstances shift dramatically.

Why Budget Flexibility Matters

Financial flexibility isn’t just convenient—it’s essential for long-term stability. According to financial experts, households that regularly review and adjust their spending plans are better equipped to handle emergencies, avoid debt, and maintain progress toward savings goals.

The core principle is simple: Your budget should serve your life, not the other way around. When major changes occur, clinging to an outdated spending plan can lead to financial stress, missed opportunities, or mounting debt.

The Foundation: Your Current Financial Snapshot

Before making any adjustments, you need to understand where you stand financially. Take stock of:

- Monthly income (all sources combined)

- Fixed expenses (rent/mortgage, insurance, loan payments)

- Variable expenses (groceries, entertainment, utilities)

- Savings and emergency funds

- Outstanding debts

- Financial obligations and goals

This baseline becomes your reference point for all future adjustments. Consider using budgeting apps like Mint, YNAB (You Need a Budget), or EveryDollar to track these numbers automatically.

How Budget Adjustment Works: The Core Framework

Successfully adapting your budget isn’t guesswork—it follows a systematic approach that works regardless of the specific life change you’re facing.

Step 1: Identify the Change and Its Financial Impact

Start by clearly defining what’s changing and how it affects your finances. Be specific and realistic about the financial implications.

For example:

- Marriage might mean combined income but also shared expenses

- Job loss means reduced or eliminated income temporarily

- A new baby means increased expenses for childcare, diapers, medical care, and more

Write down all the obvious impacts first, then take time to consider indirect effects. A new baby doesn’t just mean buying diapers—it might also mean one parent reducing work hours, increased health insurance costs, or moving to a larger apartment.

Step 2: Recalculate Your Income and Expenses

With the change identified, it’s time to crunch new numbers.

Income adjustments: Calculate your new total household income. If you’re facing job loss, include unemployment benefits, severance pay, or any side income. For marriage, combine both incomes and decide how you’ll manage joint versus separate finances.

Expense adjustments: List all new expenses and identify which existing expenses will change. Some costs might increase (groceries for a larger family), while others might decrease (dating expenses after marriage).

Don’t forget to account for one-time costs associated with the change itself—wedding expenses, moving costs, or baby gear purchases.

Step 3: Prioritize Your Spending Categories

Not all expenses are created equal. Use this hierarchy to guide your decisions:

- Essential needs: Housing, utilities, basic food, necessary medications

- Financial obligations: Debt payments, insurance premiums

- Important but flexible: Transportation, phone service, clothing

- Quality of life: Entertainment, dining out, hobbies

- Future goals: Retirement savings, vacation funds, investment contributions

During tight financial periods, you may need to temporarily pause category 5, reduce category 4, and find creative solutions for category 3.

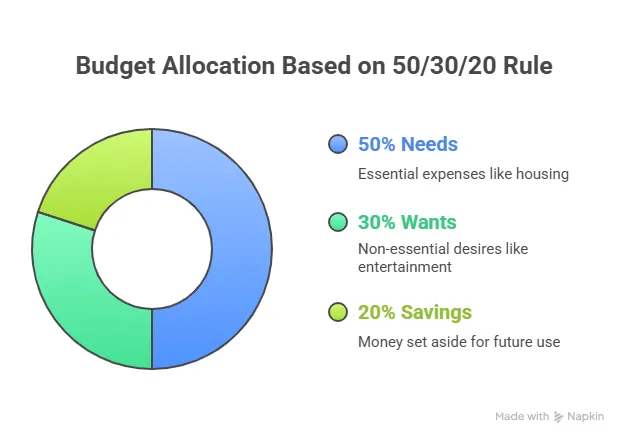

Step 4: Create Your Adjusted Budget Plan

Now draft your revised budget using the 50/30/20 rule as a flexible guideline:

- 50% for needs (essentials and obligations)

- 30% for wants (discretionary spending)

- 20% for savings and debt repayment

These percentages aren’t absolute—they’re starting points. During job loss, you might shift to a 70/10/20 model, prioritizing essentials while cutting discretionary spending. With a new high-paying job, you might increase savings to 30%.

Step 5: Implement, Monitor, and Refine

Put your adjusted budget into action, but stay vigilant. Track your actual spending against your plan for at least three months. Life changes often come with unexpected financial surprises, so be prepared to make micro-adjustments along the way.

Set calendar reminders to review your budget weekly during the first month, then monthly once things stabilize.

Common Life Changes and Budget Adjustment Strategies

Let’s explore practical, actionable strategies for the three most significant life transitions: marriage, job loss, and having children.

Adjusting Your Budget for Marriage

Marriage brings two financial lives together, which requires thoughtful planning and open communication.

Financial conversation starters: Before adjusting your budget, discuss your financial values, spending habits, debt situations, and long-term goals with your partner. These conversations prevent future conflicts and establish shared expectations.

Combining finances strategically: Decide on your approach—fully combined, completely separate, or a hybrid model. Many couples find success with the “yours, mine, and ours” method: maintain individual accounts for personal spending while contributing proportionally to a joint account for shared expenses.

Budget adjustments to make:

- Housing costs: Can you reduce expenses by living together or do you need to upgrade to accommodate both of you?

- Insurance: Investigate marriage discounts on car and home insurance, and optimize health insurance coverage by choosing the best plan between both employers

- Utilities and subscriptions: Eliminate duplicate streaming services, memberships, and subscriptions

- Food budget: Cooking together typically costs less per person than two people eating separately

- Transportation: Consider whether you can function as a one-car household

- Debt repayment: Create a unified debt elimination strategy, tackling high-interest debt first

- Emergency fund: Build toward 3-6 months of combined living expenses

- Future goals: Align savings for home down payment, children, or other shared dreams

Tax considerations: Marriage affects your tax filing status. Consult with a tax professional to optimize withholdings and understand how combining incomes impacts your tax bracket.

Adjusting Your Budget After Job Loss

Job loss ranks among the most financially stressful life events, but a strategic budget adjustment can help you navigate this challenge successfully.

Immediate actions (Days 1-7):

- File for unemployment benefits immediately—don’t wait

- Calculate your reduced income including unemployment, severance, and spouse’s income

- Review your emergency fund and determine how many months of expenses it covers

- Contact creditors to explain your situation and explore hardship programs

- Pause non-essential subscriptions and discretionary spending immediately

Short-term budget strategy (Weeks 2-8):

Slash discretionary spending: Cut entertainment, dining out, subscription services, and non-essential shopping to nearly zero. This isn’t permanent—it’s a strategic pause while you regain financial footing.

Reduce variable expenses:

- Switch to generic brands for groceries

- Implement meal planning to reduce food waste

- Lower utility costs by adjusting thermostats and reducing usage

- Cancel or pause gym memberships in favor of free outdoor exercise

- Cut cable in favor of one budget streaming service

Protect essential expenses: Continue paying rent/mortgage, utilities, insurance, and minimum debt payments. If you can’t afford minimums, contact lenders immediately to discuss options.

Generate additional income: While job hunting, consider temporary income sources like gig economy work (delivery driving, task services), selling unused items, or freelancing in your skill area.

Long-term considerations (Months 3+):

If unemployment extends beyond a few months, more substantial changes may be necessary:

- Refinance loans to lower monthly payments

- Negotiate lower rent or consider temporary housing with family

- Apply for assistance programs (SNAP, Medicaid, utility assistance)

- Withdraw from retirement accounts only as a last resort (penalties and taxes apply)

Recovery phase: Once re-employed, resist the urge to immediately return to pre-job-loss spending. Rebuild your emergency fund first, then gradually reintroduce discretionary spending.

Adjusting Your Budget for Children

The financial impact of children extends far beyond diapers and formula. Budget adjustments for parenthood require both immediate changes and long-term planning.

Before baby arrives:

Build a baby fund: Target $3,000-$5,000 for one-time expenses like furniture, car seat, stroller, and initial supplies. Buy secondhand when safe (clothes, toys) and new for safety-critical items (car seats, cribs).

Review and adjust insurance: Add baby to health insurance during the special enrollment period, increase life insurance coverage for both parents, and consider starting a college savings plan (529 account).

Test-run the new budget: If a parent will reduce hours or stop working, practice living on the reduced income for 2-3 months before baby arrives, banking the difference as additional savings.

Immediate budget changes (Year 1):

- Childcare: Often the largest new expense, ranging from $700-$2,000+ monthly depending on your location and whether you choose daycare, nanny, or family care

- Diapers and supplies: Budget $70-$80 monthly for diapers, wipes, and toiletries

- Formula or food: If not breastfeeding, formula costs $150-$300 monthly

- Healthcare: Increased copays, medications, and well-child visits typically add $100-$200 monthly

- Clothing: Babies outgrow clothes quickly—budget $30-$50 monthly, buying secondhand when possible

Offsetting strategies:

- Accept hand-me-downs from friends and family

- Join baby item swap groups on social media

- Use cloth diapers to reduce long-term costs

- Breastfeed if possible (can save $1,800+ annually)

- Shop consignment sales for baby gear

Long-term adjustments (Years 2+):

As children grow, your budget priorities shift:

- Childcare costs may decrease as children enter school but consider after-school care expenses

- Activity and extracurricular costs increase (sports, music lessons, clubs)

- Food budgets grow substantially as kids develop bigger appetites

- Education expenses emerge (school supplies, field trips, eventually college)

- Housing needs may require upgrades for more space

College savings strategy: Even $50-$100 monthly starting early can grow significantly through compound interest. Start small if needed—something is always better than nothing.

Balance family priorities: While providing for children is crucial, don’t completely sacrifice retirement savings. Your kids can borrow for college, but you can’t borrow for retirement.

Practical Money Management Tips for Life Transitions

Beyond specific scenarios, these universal strategies help any budget adjustment succeed.

Build and Protect Your Emergency Fund

An emergency fund is your financial shock absorber. Target 3-6 months of essential expenses, keeping the money in a high-yield savings account that’s accessible but not too convenient to raid.

Start small if necessary—even $500 provides breathing room for minor emergencies. Automate deposits by treating savings as a non-negotiable bill.

Use Budgeting Tools and Apps

Technology makes budget tracking significantly easier. Popular options include:

- Mint: Free, automatically tracks spending across accounts

- YNAB: Focuses on “giving every dollar a job,” excellent for intentional budgeting

- EveryDollar: Simple interface based on the zero-based budgeting method

- PocketGuard: Shows how much disposable income you have after bills and goals

- Spreadsheets: Google Sheets or Excel templates offer maximum customization

Choose one system and commit to it for at least three months before switching.

Communicate with Your Partner or Household

If you share finances, regular money conversations prevent conflict and keep everyone aligned. Schedule monthly “money dates” to review spending, discuss concerns, and celebrate progress.

Make it constructive rather than accusatory—focus on “we” and “our” rather than “you” statements.

Stay Flexible and Patient

Budget adjustments rarely work perfectly on the first attempt. Give yourself grace during the learning process, and remember that financial stability is built through consistent effort over time, not overnight perfection.

Seek Professional Guidance When Needed

Consider consulting a fee-only financial planner for major life changes, especially if you’re dealing with complex situations like significant debt, inheritance, or major career changes. Many planners offer one-time consultations at reasonable rates.

Frequently Asked Questions

How often should I adjust my budget?

Review your budget monthly at minimum, but make formal adjustments whenever significant life changes occur. Minor tweaks based on spending patterns can happen as needed, while major overhauls typically align with life transitions like those discussed in this guide.

What if my income is irregular or unpredictable?

Use the “base budget” method: calculate your minimum essential expenses, then build your budget on your lowest expected monthly income. When higher-income months occur, allocate extra toward savings, debt, or financial goals rather than increasing lifestyle spending.

How do I budget when both positive and negative changes happen simultaneously?

Focus on the net effect on your finances. For example, if you get married (often a positive financial change due to shared expenses) but also have a baby (increases expenses), calculate the combined impact on income and expenses, then build your budget around that new reality.

Can I still save money during financial difficulties like job loss?

While challenging, try to maintain at least minimal savings contributions even during hardship if possible. This might mean saving just $25-$50 monthly, but it maintains the habit and provides psychological benefits. However, if your situation is truly dire, temporarily pausing savings to cover essentials is acceptable—financial recovery isn’t linear.

What percentage of income should go to childcare?

Financial experts typically recommend keeping childcare costs under 10% of gross household income, though the national average is closer to 15-20%. If childcare exceeds 25% of your income, it may be worth exploring alternatives like one parent staying home temporarily, family care arrangements, or finding a work-from-home position with flexible hours.

Should I reduce retirement contributions during life changes?

This depends on the situation. During job loss, you may need to temporarily suspend contributions. However, for marriage or children, try to maintain at least enough contributions to capture your full employer match—that’s free money you don’t want to sacrifice. If you must reduce contributions, treat it as temporary and increase again as soon as financially feasible.

How do I handle disagreements with my spouse about budget adjustments?

Approach money discussions as partners solving a problem together, not adversaries. Use “I feel” statements, focus on shared goals, and consider compromise solutions. If conflicts persist, a few sessions with a financial therapist or counselor can provide tools for productive money communication.

Taking Control of Your Financial Future

Adjusting budgets through life changes isn’t just about surviving transitions—it’s about building a resilient financial foundation that supports your evolving life. Whether you’re blending finances with a partner, navigating unemployment, or welcoming children, the strategies outlined in this guide provide a roadmap for maintaining financial stability.

Remember that perfect budgeting doesn’t exist. What matters is consistent effort, honest assessment of your situation, and willingness to adapt as circumstances change. Start with one small adjustment today, track your progress, and build from there.

Your financial journey is uniquely yours, shaped by your specific circumstances, values, and goals. By mastering the skill of budget adjustment, you’re equipping yourself with one of the most powerful tools for long-term financial security—the ability to adapt and thrive regardless of what life brings your way.

Ready to take the next step? Pull out your current budget (or create one if you haven’t), identify the life change you’re facing, and implement one adjustment strategy from this guide this week. Financial transformation begins with a single intentional action.