How to Save Money on a Tight Budget: A Complete Guide to Building Financial Security

Living paycheck to paycheck can feel overwhelming. Every unexpected expense—a car repair, a medical bill, or even a higher-than-usual electricity bill—can throw your entire month into chaos. If you’re wondering how to save money on a tight budget, you’re not alone. Millions of Americans face this challenge daily, feeling trapped between mounting bills and shrinking paychecks.

But here’s the truth: saving money isn’t just for people with high incomes. Even when your budget feels impossibly tight, small, strategic changes can create breathing room and help you build genuine financial security. This comprehensive guide will walk you through practical, proven strategies that work in the real world—not just in theory.

Whether you’re earning minimum wage, supporting a family on one income, or recovering from financial setbacks, you’ll discover actionable steps to save money without sacrificing everything that brings you joy. Let’s transform your relationship with money, one realistic strategy at a time.

Understanding Your Financial Starting Point

Before you can save effectively, you need to understand exactly where your money goes. Most people significantly underestimate their spending, which makes saving feel impossible when it’s actually within reach.

Track Every Dollar for 30 Days

Grab a notebook, download a free budgeting app like Mint or EveryDollar, or create a simple spreadsheet. For the next month, record every single purchase—from your rent payment to that $2 coffee. This isn’t about judgment; it’s about awareness.

You’ll likely discover “spending leaks”—those small, frequent purchases that seem insignificant individually but add up dramatically over time. That daily energy drink habit? It could be costing you $150 monthly. Those spontaneous Target runs? Potentially hundreds of dollars you didn’t realize were disappearing.

Calculate Your True Income vs. Expenses

List your actual take-home pay (after taxes) and compare it against your total monthly expenses. Be brutally honest here. Include everything: housing, utilities, transportation, food, insurance, debt payments, subscriptions, entertainment, personal care, and those miscellaneous expenses that somehow always appear.

If your expenses exceed your income, you’re operating in survival mode, and your first priority is closing that gap. If you have a small surplus, excellent—you already have money to allocate toward savings, even if it doesn’t feel that way.

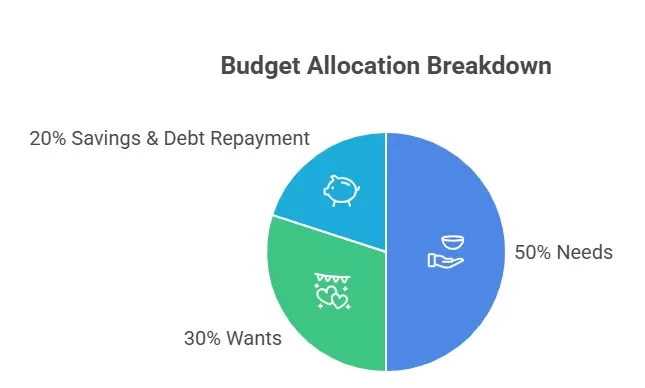

The Foundation: Creating a Realistic Budget

A budget isn’t a financial prison—it’s a plan that tells your money where to go instead of wondering where it went. When you’re on a tight budget, this plan becomes your roadmap to financial stability.

Use the Zero-Based Budget Method

With zero-based budgeting, you assign every dollar a job before the month begins. Your income minus your expenses and savings should equal zero. This doesn’t mean spending everything—it means intentionally allocating funds to categories, including savings, before the month starts.

Start with your “Four Walls”: food, shelter (including utilities), basic transportation, and basic clothing. These non-negotiables get funded first. Everything else comes afterward.

Build Categories That Reflect Your Reality

Don’t create a fantasy budget based on who you wish you were. Create one based on your actual life and habits, then adjust from there. Include categories for:

- Fixed expenses (rent, insurance, debt payments)

- Variable necessities (groceries, gas, utilities)

- Periodic expenses (annual subscriptions, car registration, holiday gifts)

- Small discretionary spending (because complete deprivation leads to budget failure)

The key is being realistic while identifying areas for improvement.

Immediate Strategies to Cut Expenses Without Suffering

Cutting expenses doesn’t mean living like a monk. It means eliminating waste and getting strategic about spending.

Slash Housing Costs Creatively

Housing typically consumes 30-40% of income, making it your biggest savings opportunity. If your rent exceeds 30% of your take-home pay, consider these options:

Get a roommate or rent out a spare room. Splitting housing costs can immediately free up hundreds of dollars monthly. Even if you value your privacy, a year of shared housing could build an emergency fund that provides long-term security.

Negotiate with your landlord. If you’ve been a reliable tenant, ask about a rent reduction in exchange for a longer lease, property maintenance tasks, or prepaying several months. The worst they can say is no.

Explore housing assistance programs. Depending on your income level, you might qualify for programs like Section 8, Low-Income Home Energy Assistance Program (LIHEAP), or local nonprofit housing support. Check with your local housing authority or visit benefits.gov.

Dramatically Reduce Food Costs

The average American household spends over $500 monthly on food, but this category has tremendous flexibility.

Master meal planning and batch cooking. Dedicate two hours on Sunday to plan your week’s meals and prep ingredients. Cook large batches of affordable staples like rice and beans, pasta dishes, stews, and casseroles. These stretch your dollars while minimizing the temptation to order takeout on busy nights.

Shop with a strategic list. Never grocery shop hungry or without a detailed list organized by store section. Buy store brands, use coupons through apps like Ibotta and Fetch, and shop sales—but only for items you actually need.

Embrace affordable protein sources. Eggs, canned tuna, chicken thighs (not breasts), dried beans, and lentils provide protein at a fraction of the cost of steak and seafood. A dozen eggs costs around $3 and provides six high-protein meals.

Cut restaurant spending by 75%. If you currently spend $200 monthly eating out, reducing this to $50 saves $150 immediately. Reserve restaurant meals for truly special occasions, and make “restaurant-quality” meals at home by finding copycat recipes online.

Eliminate Subscription Creep

Americans typically have 12 paid subscriptions, and many have forgotten what they’re even paying for. Review your bank statements and cancel anything you don’t actively use weekly.

Streaming services: Keep one, rotate seasonally, or share accounts with family members (where allowed by terms of service). Consider free alternatives like Tubi, Pluto TV, or your local library’s streaming services.

Gym memberships: If you’re not going at least twice weekly, cancel it. Use free YouTube fitness videos, run outdoors, or check if your local community center offers affordable recreation programs.

Subscriptions you forgot about: That meditation app you used once? The meal kit service you meant to cancel? The software trial that converted to paid? Eliminate them all.

Revolutionize Transportation Spending

Transportation is typically the second-largest expense category, but it’s also loaded with savings opportunities.

If possible, go car-free or one-car. This isn’t realistic for everyone, but if you live in an area with decent public transit or can bike/walk to work, selling a car eliminates payments, insurance, maintenance, and fuel costs—potentially saving $500+ monthly.

Refinance your car loan. If your credit has improved since you bought your car, refinancing could lower your interest rate and monthly payment.

Maintain your vehicle religiously. Regular oil changes, tire rotations, and addressing small issues before they become major problems will save thousands in repair costs. A $40 oil change beats a $3,000 engine repair.

Reduce insurance costs without sacrificing coverage. Shop around annually using comparison sites. Ask about discounts for safe driving, bundling policies, paying in full, or taking defensive driving courses. Raising your deductible slightly can also lower premiums—just ensure you could afford the higher deductible in an emergency.

Building Savings When Money is Extremely Tight

Even saving $5 weekly matters. Small amounts compound over time and, more importantly, build the psychological habit of saving.

Start With a Micro Emergency Fund

Your first goal is saving $500-$1,000. This modest amount won’t cover major emergencies, but it will handle most small crises—a car battery, a minor medical copay, or a necessary household repair—without derailing your finances.

Break this into manageable milestones. Saving $1,000 feels overwhelming. Saving $50 doesn’t. Celebrate every $50 or $100 milestone to maintain motivation.

Automate the Process

Set up an automatic transfer of whatever amount you can consistently afford—even $5 or $10—from checking to savings the day after each payday. Treating savings as a non-negotiable “bill” ensures it happens before discretionary spending consumes everything.

Open a separate savings account, preferably at a different bank or credit union than your checking account. This creates a psychological barrier against impulse withdrawals. Look for high-yield savings accounts that earn actual interest, like those from Ally, Marcus by Goldman Sachs, or many credit unions.

Apply the “Save the Difference” Method

When you cut an expense, immediately transfer that amount to savings. Cancelled a $15 subscription? Transfer $15 to savings. Spent $20 less on groceries this week? Move that $20 into your emergency fund.

This strategy accelerates savings while reinforcing positive financial behavior.

Use Financial Windfalls Strategically

Tax refunds, work bonuses, birthday money, or any unexpected income should be divided: at least 50% to savings or debt payoff, with the remainder for something that genuinely improves your life. This balance prevents the deprivation that leads to financial burnout while still advancing your goals.

Increasing Income on Your Terms

Sometimes cutting expenses only goes so far. Strategically increasing income—even modestly—can dramatically improve your financial situation.

Monetize Skills You Already Have

You don’t need special training to earn extra money. Can you clean, organize, babysit, tutor, walk dogs, or do yard work? Advertise through local Facebook groups, Nextdoor, or sites like Care.com and Rover.

Gig economy opportunities like DoorDash, Instacart, or Uber offer flexible earning potential. Run the numbers carefully to ensure the income exceeds vehicle costs and time investment, but many people successfully add $200-$500 monthly through strategic gig work.

Sell Items You No Longer Need

Most households have hundreds or thousands of dollars worth of unused items. Clothes you haven’t worn in years, electronics gathering dust, furniture taking up space—these can become immediate savings.

Use Facebook Marketplace for large items, Poshmark or Mercari for clothing, and eBay for electronics or collectibles. Dedicate one weekend to identifying everything you can sell, and commit that income entirely to your emergency fund.

Ask for a Raise at Your Current Job

If you’ve been at your job for over a year, consistently perform well, and haven’t received a raise, schedule a conversation with your manager. Research industry salary standards for your role and location, document your contributions and achievements, and make a clear case for increased compensation.

The answer might be no, but asking costs nothing. Even a 3% raise on a $35,000 salary adds over $1,000 annually—nearly $100 monthly that could transform your budget.

Avoiding Common Money-Saving Mistakes

Well-intentioned strategies can backfire if you’re not careful.

Don’t Cut Everything That Brings Joy

Extreme frugality is unsustainable. If you eliminate every small pleasure, you’ll eventually rebel spectacularly, potentially undoing months of progress. Budget a modest amount—$20, $50, whatever you can reasonably afford—for guilt-free spending on things that genuinely improve your quality of life.

Maybe it’s your favorite coffee once weekly, a streaming service you actually use, or craft supplies for your hobby. This “pressure release valve” keeps your budget sustainable long-term.

Avoid the “Cheap Now, Expensive Later” Trap

Buying the cheapest option isn’t always economical. A $30 pair of work shoes that lasts six months costs more than $60 shoes lasting two years. Focus on value and cost-per-use, not just initial price.

For essentials you use frequently, saving up for the quality option usually saves money long-term while reducing frustration.

Don’t Ignore Debt

Ignoring debt never makes it disappear—it only makes it worse. Minimum payments keep you trapped in interest charges for decades. Once you’ve established your micro emergency fund, aggressively attack high-interest debt using the debt avalanche (highest interest first) or debt snowball (smallest balance first) method.

Even an extra $20 monthly toward debt accelerates your payoff timeline and reduces total interest paid.

Creating a Sustainable Financial Mindset

Saving money successfully requires psychological shifts, not just tactical changes.

Reframe Your Relationship With Money

Money isn’t inherently good or evil—it’s a tool. You’re not “bad with money” or “financially cursed.” You’re learning skills most Americans never develop. Every positive financial decision, no matter how small, represents progress.

Replace shame with curiosity. Instead of “Why did I waste money on that?” ask “What triggered that purchase, and what can I do differently next time?”

Celebrate Progress, Not Perfection

You’ll have setbacks. You’ll make impulse purchases or face unexpected expenses that drain your savings. This is normal. What matters is your overall trajectory, not individual mistakes.

Saved your first $100? That deserves celebration. Stayed under budget on groceries three weeks in a row? Acknowledge that achievement. Small wins build momentum toward larger goals.

Connect Saving to Your “Why”

Saving feels easier when it’s connected to meaningful goals. Are you saving to escape the anxiety of living paycheck to paycheck? To create opportunities for your children? To eventually take a vacation? To achieve career flexibility?

Write down your specific “why” and revisit it when motivation wanes. Your emergency fund isn’t just money in an account—it’s peace of mind, security, and future possibilities.

Taking Your First Steps Today

Saving money on a tight budget isn’t easy, but it’s absolutely possible. Millions of people start exactly where you are and successfully build financial stability through consistent effort and smart decisions.

Your action plan for this week:

- Track every expense for the next 30 days starting today

- Calculate your current income minus expenses to identify your starting point

- Cancel one unused subscription before the next billing cycle

- Set up automatic savings transfer of any amount you can consistently afford

- Choose one major expense category to reduce and implement one specific strategy

You don’t need to implement everything simultaneously. Start with strategies that feel most achievable and build from there. Each small change creates momentum for the next one.

Remember: you’re not just saving money—you’re building financial skills that will benefit you for life. The stress you feel about money today can transform into confidence and security with consistent effort over time.

Your financial situation may be tight, but your potential isn’t. Every dollar you save represents freedom, choice, and a stronger foundation for your future. You’ve got this, and you’re already taking the crucial first step by seeking knowledge and solutions.

Start today. Start small. Start where you are. Your future self will thank you for the decision you’re making right now.