Where Should You Live? Comparing Cost of Living Like a Pro

Choosing where to live is one of the biggest financial decisions you’ll ever make. Whether you’re fresh out of college, switching jobs, or simply craving a change of scenery, understanding how to compare cost of living between different cities can save you thousands of dollars—and a lot of stress.

But here’s the thing: most people approach this decision all wrong. They see a higher salary in a big city and jump at the opportunity, only to realize their paycheck disappears faster than ice cream on a summer day. Or they choose a place based purely on “vibes” without crunching the numbers, leading to financial regret down the road.

Don’t worry—you’re about to learn exactly how to compare cost of living like a pro. By the end of this guide, you’ll have a clear, step-by-step system for evaluating any city or town and making a confident decision that aligns with both your lifestyle and your wallet.

Why Cost of Living Matters More Than Your Salary

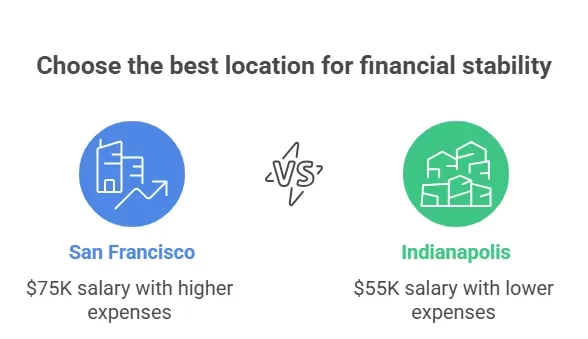

Let’s start with a reality check. A $75,000 salary in San Francisco is not the same as $75,000 in Austin, Texas—not even close. After accounting for housing, taxes, transportation, and daily expenses, that San Francisco salary might leave you with less disposable income than a $55,000 salary in a mid-sized Midwestern city.

This is why understanding cost of living is crucial. It’s not about how much you earn; it’s about how much you keep and what quality of life that money buys you. Cost of living encompasses everything from rent and groceries to healthcare and entertainment. When you compare these factors across different locations, you gain a realistic picture of where your money will stretch furthest and where you’ll actually enjoy living.

Understanding the Core Components of Cost of Living

Before you start comparing cities, you need to understand what actually makes up the cost of living. Think of it as a pie chart of your monthly expenses—some slices are bigger than others, and they vary dramatically depending on where you live.

Housing: Your Biggest Expense

For most Americans, housing consumes 30-40% of their income. This includes rent or mortgage payments, property taxes, insurance, and utilities. In cities like New York or Los Angeles, a one-bedroom apartment can easily cost $3,000+ per month. Meanwhile, in cities like Oklahoma City or Louisville, that same money could rent you a spacious three-bedroom house with a yard.

When comparing housing costs, don’t just look at rent prices. Consider property taxes if you’re buying, average utility costs (which vary by climate), and whether you’ll need renters or homeowners insurance. Also think about the trade-offs: are you willing to have roommates, live farther from downtown, or accept a smaller space to save money?

Transportation: The Hidden Budget Killer

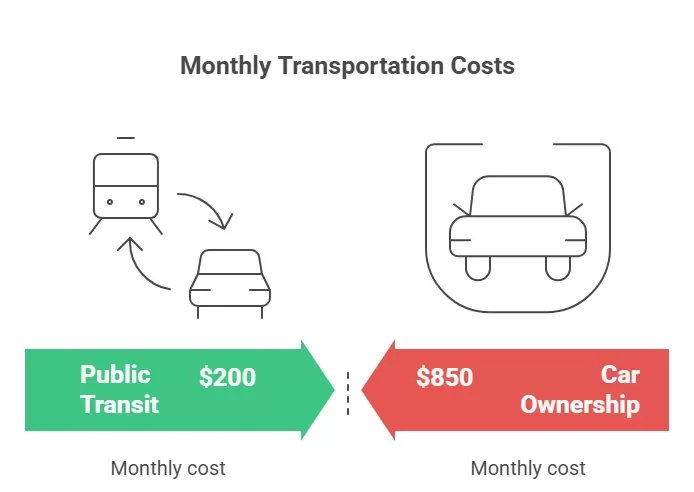

Transportation costs vary wildly depending on whether you need a car. In cities with excellent public transit like New York, Chicago, or Washington D.C., you might spend $100-150 monthly on transit passes. But in sprawling cities like Houston or Phoenix, you’ll likely need a car, which means factoring in car payments, insurance, gas, maintenance, and parking—easily $500-800+ per month.

Don’t forget to consider your commute distance and time. Living in a cheaper suburb might seem smart until you calculate that you’re spending $300 monthly on gas and two hours daily in traffic. That’s money and time you’re not getting back.

Food and Groceries: More Than Just Your Appetite

Grocery prices can vary by 20-30% between different cities. A gallon of milk might cost $2.50 in the Midwest but $4.50 in Hawaii or Alaska. Restaurant prices show even bigger differences—a casual dinner out might be $15 per person in Omaha but $30+ in Seattle or Boston.

Consider your lifestyle here. If you eat out frequently, you’ll feel the pinch more in expensive cities. If you cook most meals at home, grocery price differences matter more than restaurant costs.

Healthcare: The Often-Overlooked Factor

Healthcare costs vary significantly by state and region due to different insurance markets, hospital systems, and state regulations. Some states have expanded Medicaid, while others haven’t. Some regions have competitive healthcare markets that drive prices down, while others are dominated by a single health system.

Research average health insurance premiums in your target cities, and if you have specific healthcare needs, check whether quality specialists and facilities are available and affordable.

Taxes: What Your Paycheck Really Looks Like

State and local taxes can dramatically affect your take-home pay. Nine states have no income tax (Alaska, Florida, Nevada, South Dakota, Tennessee, Texas, Washington, and Wyoming, plus New Hampshire which only taxes dividends and interest). Others, like California and New York, have top rates exceeding 10%.

But don’t just focus on income tax. Some no-income-tax states compensate with higher property taxes or sales taxes. Texas, for example, has no income tax but some of the highest property taxes in the nation. You need to look at your total tax burden, not just one piece.

Step-by-Step: How to Compare Cost of Living Between Cities

Now that you understand the components, let’s walk through the actual comparison process. This step-by-step approach will give you concrete numbers to work with, not just guesswork.

Step 1: Use Cost of Living Calculators

Start with online cost of living calculators—they’re free, fast, and surprisingly accurate. The best ones include:

- NerdWallet’s Cost of Living Calculator: Great for comparing overall expenses

- Numbeo: Crowd-sourced data with detailed breakdowns

- BestPlaces Cost of Living: Includes quality of life factors beyond just money

- PayScale Cost of Living Calculator: Particularly useful if you’re comparing job offers

Enter your current city and salary, then compare it to potential new cities. These calculators will show you how much you’d need to earn in the new location to maintain your current lifestyle. They typically adjust for housing, food, transportation, utilities, and healthcare.

For example, if you earn $60,000 in Atlanta and are considering a move to Denver, the calculator might show you’d need $68,000 in Denver to maintain the same standard of living. This doesn’t mean you shouldn’t move—it means you need to account for that $8,000 difference.

Step 2: Research Housing Costs in Detail

Don’t rely solely on averages—dig into actual listings. Spend time on Zillow, Apartments.com, or Realtor.com searching for places that match what you’d actually want to rent or buy. Look at different neighborhoods within the city, and note the trade-offs.

Create a simple spreadsheet with columns for:

- Location/neighborhood

- Monthly rent or mortgage estimate

- Average utilities (search “[city name] average utilities” to find local data)

- Commute distance to work or downtown

- Neighborhood amenities and safety ratings

This gives you real numbers, not just citywide averages that might not reflect where you’d actually live.

Step 3: Calculate Transportation Costs Realistically

Be honest about your transportation needs. Will you need a car, or can you rely on public transit, biking, or walking?

If you need a car, calculate:

- Car payment (if applicable): $___

- Insurance (get actual quotes for your new city): $___

- Gas (estimate based on your commute and current driving habits): $___

- Maintenance and repairs (budget at least $100/month): $___

- Parking (if you’ll need to pay for it): $___

If using public transit:

- Monthly pass cost: $___

- Occasional rideshare/taxi: $___

Many people underestimate car costs. The AAA estimates that owning a vehicle costs Americans an average of $9,500 annually, or about $800 per month. If you can avoid car ownership, that’s substantial savings.

Step 4: Factor in Lifestyle and Discretionary Spending

Your lifestyle significantly impacts your cost of living. Two people earning the same salary in the same city can have vastly different expenses based on their choices.

Consider:

- How often do you eat out or order delivery?

- Do you enjoy nightlife, concerts, or entertainment?

- Are fitness classes, gym memberships, or outdoor activities important to you?

- Do you have expensive hobbies?

- How often do you travel or visit family?

Research prices for activities you regularly enjoy in your target cities. A yoga studio membership might be $100/month in Kansas City but $200/month in San Diego. Concert tickets, ski passes, beach parking—whatever matters to your lifestyle, price it out.

Step 5: Run the Complete Numbers

Now bring it all together in a comprehensive budget comparison. Create a monthly budget for each city you’re considering:

City A Monthly Budget:

- Housing: $___

- Utilities: $___

- Transportation: $___

- Groceries: $___

- Dining out: $___

- Healthcare/insurance: $___

- Taxes (estimated monthly withholding): $___

- Entertainment/lifestyle: $___

- Savings goals: $___

- Total: $___

City B Monthly Budget:

- [Same categories]

- Total: $___

Compare your projected income in each location against these budgets. Which city leaves you with more disposable income? Which one lets you save more toward your goals?

Beyond the Numbers: Quality of Life Factors

Cost of living isn’t just about dollars and cents—it’s about the life those dollars buy you. A lower cost of living means nothing if you’re miserable in your new city.

Consider these qualitative factors:

Climate and Weather: Can you handle harsh winters, intense heat, or constant rain? Climate affects not just your happiness but also your expenses (heating, cooling, appropriate clothing).

Job Market and Career Growth: Is there a strong job market in your field? What if you need to find a new job in a year or two? Career opportunities matter for long-term financial health.

Social and Cultural Fit: Will you find your community there? Are there activities, restaurants, cultural events, and social scenes that align with your interests?

Safety and Crime Rates: Research neighborhood safety using sites like NeighborhoodScout. Your peace of mind has value.

Education and Schools: If you have or plan to have children, school quality is crucial. Even if you don’t, good schools typically indicate stable, well-funded communities.

Proximity to Family and Friends: Long-distance relationships have emotional and financial costs. Factor in travel expenses and the value of having a support system nearby.

Common Mistakes to Avoid

Even with all this information, people still make predictable mistakes when comparing cost of living. Here’s what to watch out for:

Mistake #1: Focusing Only on Housing Costs Yes, housing is your biggest expense, but it’s not your only one. Don’t choose a city solely because rent is cheap if everything else costs significantly more.

Mistake #2: Ignoring State and Local Taxes That higher salary in a high-tax state might leave you with less take-home pay than a smaller salary in a tax-friendly state. Always calculate after-tax income.

Mistake #3: Underestimating the Hidden Costs Moving costs, deposits, new furniture, establishing services—relocating isn’t free. Budget $3,000-5,000 for the transition itself.

Mistake #4: Not Visiting First Never move somewhere you’ve never visited. Spend at least a long weekend exploring different neighborhoods, experiencing the commute, and getting a feel for daily life.

Mistake #5: Forgetting Your Long-Term Goals Choose a location that supports your 5-10 year goals, not just your immediate situation. If you want to buy a house someday, can you realistically save for a down payment in your target city?

Taking Action: Your Next Steps

You now have a professional framework for comparing cost of living. Here’s your action plan:

This Week:

- Use at least two cost of living calculators to compare your top 2-3 cities

- Research actual housing options in those cities on rental or real estate sites

- Calculate realistic monthly budgets for each location

This Month:

- Get insurance quotes (car, health, renters/homeowners) for your target cities

- Join local online communities or subreddits for those cities to ask residents questions

- If possible, plan a visit to experience the city firsthand

Before You Decide:

- Create a comparison spreadsheet with both financial and quality-of-life factors

- Run different scenarios (best case, worst case, realistic case)

- Talk to people who already live in your target cities

- Trust your gut—numbers matter, but so does where you feel at home

Conclusion: Making Your Choice with Confidence

Comparing cost of living doesn’t have to be overwhelming. With the right tools, a systematic approach, and honest self-reflection about your priorities, you can make an informed decision about where to live.

Remember: there’s no single “best” place to live. The best place for you is where your finances align with your lifestyle, career goals, and personal happiness. Some people thrive in expensive cities because the career opportunities justify the cost. Others find freedom and financial security in lower-cost areas that let them save aggressively and enjoy life without financial stress.

What matters most is that you make your decision with eyes wide open, armed with real data and a clear understanding of trade-offs. Use this guide as your roadmap, do your homework, and trust that you’re making a smart, well-informed choice.

Your next chapter is waiting—and now you know exactly how to choose where to write it.