How Rich Are You Really? Learn to Calculate Your Net Worth

Have you ever wondered where you truly stand financially? Not just how much money sits in your checking account, but your actual wealth? You’re not alone. Most Americans have never calculated their net worth, yet this single number reveals more about your financial health than your salary ever could.

Whether you’re just starting your career, planning for retirement, or simply curious about your financial position, understanding your net worth is the first step toward building lasting wealth. The good news? Calculating it is surprisingly simple, and you can do it in less than 30 minutes.

In this comprehensive guide, I’ll walk you through everything you need to know about net worth—what it means, why it matters, and exactly how to calculate yours step by step. By the end, you’ll have a clear picture of your financial standing and a roadmap for improving it.

What Is Net Worth? (And Why Should You Care?)

Net worth is the clearest snapshot of your financial health. Simply put, it’s the total value of everything you own (your assets) minus everything you owe (your liabilities).

Think of it this way: If you sold everything you own today and paid off all your debts, how much money would you have left? That’s your net worth.

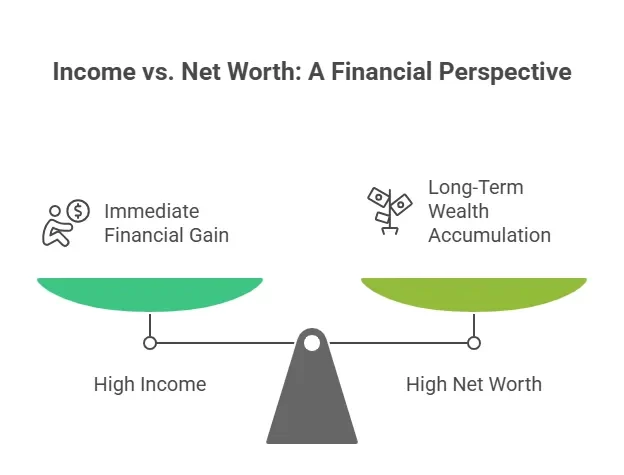

Unlike your income—which only shows how much you earn—net worth reveals how much wealth you’ve actually built. You could earn $200,000 a year but have a negative net worth if you’re drowning in debt. Conversely, someone earning $60,000 annually might have a net worth of $500,000 through smart saving and investing.

Why Net Worth Matters More Than Income

Your salary doesn’t tell the whole story. Consider two people: Sarah earns $150,000 but has $200,000 in student loans and credit card debt. Meanwhile, James earns $70,000, owns a modest home with significant equity, and has $100,000 in retirement savings. Despite earning less, James has built substantially more wealth.

Tracking your net worth helps you:

- Measure real financial progress beyond just your paycheck

- Make smarter money decisions about spending, saving, and investing

- Set realistic financial goals based on where you actually stand

- Identify problem areas draining your wealth

- Build confidence as you watch your number grow over time

Understanding the Net Worth Formula

Before we dive into calculations, let’s break down the basic formula:

Net Worth = Total Assets – Total Liabilities

It’s that straightforward. But understanding what counts as an asset versus a liability is crucial for accuracy.

What Are Assets?

Assets are anything you own that has monetary value. They fall into several categories:

Liquid Assets (easily converted to cash):

- Cash in checking and savings accounts

- Money market accounts

- Certificates of deposit (CDs)

- Stocks, bonds, and mutual funds

- Cryptocurrency holdings

Retirement Assets:

- 401(k) or 403(b) accounts

- Traditional and Roth IRAs

- Pension plans

- SEP-IRAs or Solo 401(k)s (for self-employed individuals)

Personal Property Assets:

- Your primary residence (current market value)

- Investment properties or rental real estate

- Vehicles (cars, motorcycles, boats)

- Jewelry and collectibles

- Electronics and furniture (if significant value)

Business Assets (if applicable):

- Business ownership equity

- Business property and equipment

What Are Liabilities?

Liabilities are your debts—money you owe to others. Common liabilities include:

- Mortgage balances on homes

- Home equity loans or lines of credit (HELOCs)

- Auto loans

- Student loans

- Credit card balances

- Personal loans

- Medical debt

- Business loans

- Tax debt

Important note: Only include the current balance you owe, not the original loan amount or total you’ll pay with interest.

Step-by-Step: How to Calculate Your Net Worth

Ready to discover your true financial position? Grab a notebook, open a spreadsheet, or use a financial tracking app. Let’s calculate your net worth together.

Step 1: List All Your Assets

Start by gathering information about everything you own. Be thorough but realistic about valuations.

Cash and Bank Accounts: Log into your online banking and write down current balances for:

- Checking accounts

- Savings accounts

- Money market accounts

- CDs

Investment Accounts: Check your brokerage statements for:

- Individual stocks

- Mutual funds

- ETFs (Exchange-Traded Funds)

- Bonds

- Cryptocurrency wallets

Retirement Accounts: Review your most recent statements for:

- 401(k) or 403(b) (include employer contributions)

- Traditional IRAs

- Roth IRAs

- SEP-IRAs or Solo 401(k)s

Real Estate: Estimate the current market value of:

- Your primary home (use Zillow, Redfin, or recent comparable sales)

- Rental properties

- Vacation homes

- Land

Vehicles: Look up current values using Kelley Blue Book (KBB) or Edmunds for:

- Cars

- Motorcycles

- Boats

- RVs

Other Valuable Assets: Include any items worth $500 or more:

- Jewelry (get appraisals for high-value pieces)

- Art and collectibles

- Antiques

- High-end electronics

Example: Let’s follow Maria, a 32-year-old marketing manager:

- Checking/Savings: $8,500

- 401(k): $47,000

- Roth IRA: $12,000

- Home value: $285,000

- Car value: $14,000

- Emergency fund (money market): $15,000

Maria’s Total Assets: $381,500

Step 2: List All Your Liabilities

Now for the less fun part—tallying up what you owe. Be honest and comprehensive.

Mortgage and Real Estate Debt: Check your most recent mortgage statement for:

- Primary mortgage balance

- Second mortgage or HELOC balance

- Investment property mortgages

Consumer Debt: Gather statements for:

- Credit card balances (all cards)

- Auto loans (remaining balance)

- Personal loans

- Buy now, pay later balances

Educational Debt: Check your student loan servicer for:

- Federal student loans

- Private student loans

Other Debts: Include:

- Medical bills

- Business loans

- Family loans

- Tax debt

Example (continued): Maria’s liabilities:

- Mortgage balance: $248,000

- Car loan: $9,200

- Credit card balance: $3,400

- Student loans: $18,500

Maria’s Total Liabilities: $279,100

Step 3: Do the Math

Now subtract your total liabilities from your total assets:

Net Worth = Total Assets – Total Liabilities

For Maria: $381,500 (assets) – $279,100 (liabilities) = $102,400 net worth

Congratulations! You’ve calculated your net worth. Whether it’s positive or negative, you now have a baseline to work from.

What Your Net Worth Really Means

Now that you have your number, what does it tell you?

Is Your Net Worth Good or Bad?

There’s no universal “good” net worth, as it depends heavily on your age, location, and life stage. However, here are some general benchmarks for Americans:

By Age (median net worth in the US):

- Under 35: $13,900

- 35-44: $91,300

- 45-54: $168,600

- 55-64: $212,500

- 65+: $266,400

Remember, these are medians—half of people have more, half have less. If your net worth is below these numbers, don’t panic. You’re taking the first step by measuring it.

What If Your Net Worth Is Negative?

A negative net worth means you owe more than you own. This is extremely common, especially for:

- Recent college graduates with student loans

- Young professionals who recently bought homes

- People recovering from medical emergencies or divorce

A negative net worth isn’t permanent—it’s a starting point. With intentional financial decisions, you can flip that number positive faster than you think.

Understanding Net Worth Growth Over Time

Your net worth will naturally increase as you:

- Pay down mortgage principal (building home equity)

- Contribute to retirement accounts

- Pay off loans and credit cards

- Invest in appreciating assets

- Increase your income and savings rate

Most financial experts recommend calculating your net worth quarterly or annually to track progress and adjust your financial strategy.

Common Net Worth Calculation Mistakes to Avoid

Don’t sabotage your accuracy with these frequent errors:

1. Using Purchase Price Instead of Current Value Your home isn’t worth what you paid for it in 2015. Your car definitely isn’t. Always use current market value.

2. Forgetting Small Accounts That old 401(k) from a previous job counts. So does the savings account you opened years ago. Hunt down every account.

3. Overvaluing Personal Belongings Your furniture and clothes have almost no resale value. Be conservative or skip items worth under $500.

4. Not Including Retirement Accounts Even though you can’t access your 401(k) without penalties, it’s still part of your net worth.

5. Counting Expected Bonuses or Raises Only include money you currently have, not what you hope to earn.

6. Forgetting Small Debts That $800 medical bill in collections? It counts. The $50 you owe your friend? Maybe include it if you’re being thorough.

How to Increase Your Net Worth: Practical Strategies

Knowing your net worth is just the beginning. Here’s how to grow it:

1. Focus on Reducing High-Interest Debt

Credit card debt can devastate net worth growth. Interest rates of 18-25% mean you’re essentially taking one step backward for every two steps forward.

Action steps:

- List debts by interest rate

- Use the avalanche method (pay highest interest first) or snowball method (pay smallest balance first)

- Consider balance transfer cards with 0% intro APR

- Negotiate lower rates with creditors

2. Increase Your Savings Rate

Even small increases make massive differences over time. Going from saving 5% to 15% of your income can add hundreds of thousands to your lifetime net worth.

Action steps:

- Automate transfers to savings on payday

- Increase 401(k) contributions by 1% annually

- Save raises and bonuses instead of spending them

- Use high-yield savings accounts (currently earning 4-5%)

3. Invest for Long-Term Growth

Cash savings alone won’t build substantial wealth due to inflation. Investing puts your money to work.

Action steps:

- Max out employer 401(k) match (it’s free money!)

- Open a Roth IRA for tax-free retirement growth

- Consider low-cost index funds for beginners

- Invest consistently, even during market downturns

4. Increase Your Income

There’s a limit to how much you can cut expenses, but no limit to earning potential.

Action steps:

- Negotiate raises at your current job

- Develop high-income skills (coding, marketing, sales)

- Start a side hustle

- Consider career advancement or job changes

5. Build Home Equity

Real estate often becomes the largest component of net worth for Americans.

Action steps:

- Make extra mortgage payments toward principal

- Avoid cash-out refinancing unless strategic

- Maintain and improve your property

- Consider house hacking (renting out rooms)

6. Track and Review Regularly

What gets measured gets improved. Regular reviews help you spot problems early and celebrate wins.

Action steps:

- Calculate net worth quarterly

- Use apps like Personal Capital, Mint, or spreadsheets

- Set annual net worth growth goals

- Adjust strategies based on what’s working

Tools and Resources for Tracking Net Worth

You don’t need fancy software to track net worth, but these tools make it easier:

Free Spreadsheet Templates:

- Google Sheets net worth tracker (free)

- Microsoft Excel personal finance templates

- Custom spreadsheets you create yourself

Financial Apps:

- Personal Capital: Free comprehensive tracking with investment analysis

- Mint: Free budgeting and net worth tracking

- YNAB (You Need A Budget): Paid but excellent for budgeting ($99/year)

- Empower: Free financial planning tools

Manual Tracking: A simple notebook works perfectly fine. Many millionaires still track finances on paper!

Real-Life Net Worth Examples

Understanding how net worth works in practice helps clarify the concept:

Example 1: The Recent Graduate

- Age: 24

- Assets: $5,000 (savings), $3,000 (car)

- Liabilities: $35,000 (student loans)

- Net Worth: -$27,000

- Strategy focus: Increase income, pay down student debt aggressively

Example 2: The Established Professional

- Age: 45

- Assets: $425,000 (home), $235,000 (retirement), $35,000 (cash/investments)

- Liabilities: $285,000 (mortgage), $15,000 (car loan)

- Net Worth: $395,000

- Strategy focus: Max out retirement contributions, increase investment allocation

Example 3: The Debt-Free Renter

- Age: 35

- Assets: $180,000 (retirement accounts), $45,000 (cash), $8,000 (car)

- Liabilities: $0

- Net Worth: $233,000

- Strategy focus: Consider real estate investment, continue aggressive investing

Each person’s situation is unique, but the principles remain the same: grow assets, reduce liabilities, track progress.

Your Net Worth Journey Starts Now

Calculating your net worth isn’t about judgment—it’s about awareness. Whether your number is $1 million or -$50,000, you now have a baseline. More importantly, you understand what drives that number and how to improve it.

Remember these key takeaways:

- Net worth = assets minus liabilities (simple but powerful)

- Track it regularly to measure real financial progress

- Focus on growth over time, not comparison with others

- Increase assets and decrease liabilities through consistent action

- Be patient—building wealth is a marathon, not a sprint

Start by calculating your net worth today. Set a calendar reminder to recalculate in three months. You’ll be amazed at how motivating it is to watch that number grow.

Your financial future is waiting. Now you know exactly where you stand—and where you’re headed next.