How Long Will It Take to Pay Off Your Credit Card? A Complete Guide

If you’re staring at your credit card statement wondering when you’ll finally be free of that balance, you’re not alone. Millions of Americans carry credit card debt, and figuring out exactly how long it will take to pay it off can feel like solving a complex puzzle. The truth is, the timeline depends on several factors—but understanding these factors puts you in control.

In this comprehensive guide, we’ll walk you through everything you need to know about credit card payoff timelines, including how to calculate your own timeline, what factors speed up or slow down your progress, and proven strategies to eliminate your debt faster than you thought possible.

Understanding Credit Card Payoff Timelines: The Basics

Before we dive into calculations, let’s establish what actually determines how long you’ll be paying off your credit card.

When you carry a balance on your credit card, you’re not just paying back what you spent—you’re also paying interest on that balance every single month. This interest compounds, meaning you’re essentially paying interest on interest if you don’t pay off your balance quickly.

The three main factors that determine your payoff timeline are:

Your current balance: The amount you currently owe on your card.

Your interest rate (APR): The annual percentage rate your card charges, which translates to a monthly interest charge.

Your monthly payment: How much you’re actually paying toward the balance each month.

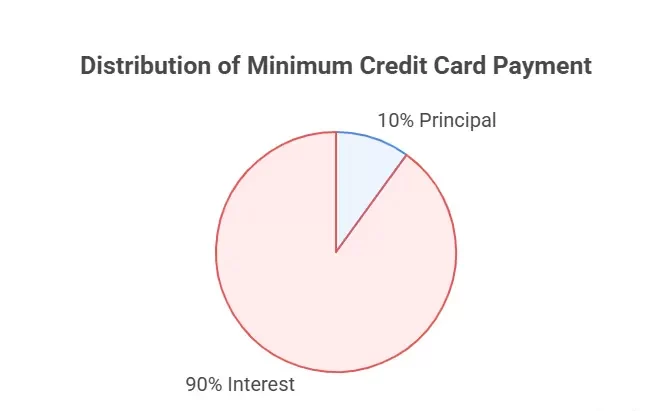

Here’s the crucial part most people miss: if you only make the minimum payment each month, you could be in debt for decades. Credit card companies typically set minimum payments at around 2-3% of your balance, which barely covers the interest charges. This keeps you in debt longer and maximizes their profit from interest charges.

How to Calculate Your Credit Card Payoff Timeline

Let’s get practical. Here’s how to figure out exactly when you’ll be debt-free based on your current situation.

The Simple Formula Method

While the exact calculation involves compound interest formulas that can get complex, here’s a simplified approach that gives you a close estimate:

Step 1: Find your monthly interest rate by dividing your APR by 12. For example, if your APR is 18%, your monthly rate is 1.5% (18 ÷ 12 = 1.5).

Step 2: Calculate your monthly interest charge by multiplying your balance by the monthly interest rate. If you owe $5,000 at 18% APR, your monthly interest is $75 ($5,000 × 0.015 = $75).

Step 3: Subtract the interest from your payment to find how much actually reduces your balance. If you pay $200 monthly, only $125 goes toward your actual debt ($200 – $75 = $125).

Step 4: Divide your total balance by the amount that reduces your principal each month for a rough estimate. In this example, $5,000 ÷ $125 = 40 months, or about 3.3 years.

However, this simplified method doesn’t account for the decreasing interest as your balance goes down, so the actual timeline is usually slightly shorter.

Real-World Examples: What Your Timeline Actually Looks Like

Let’s look at three common scenarios to see how different payment amounts dramatically affect your timeline:

Scenario 1: The Minimum Payment Trap

Balance: $5,000 APR: 18% Monthly Payment: $100 (minimum payment) Time to Pay Off: 7 years and 10 months Total Interest Paid: $4,311

In this scenario, you’d pay nearly as much in interest as your original debt!

Scenario 2: The Moderate Approach

Balance: $5,000 APR: 18% Monthly Payment: $200 Time to Pay Off: 2 years and 11 months Total Interest Paid: $1,934

Doubling your payment cuts your timeline by nearly 5 years and saves you over $2,000 in interest.

Scenario 3: The Aggressive Strategy

Balance: $5,000 APR: 18% Monthly Payment: $400 Time to Pay Off: 1 year and 2 months Total Interest Paid: $565

Quadrupling the minimum payment gets you out of debt in just over a year and saves you nearly $4,000 in interest compared to minimum payments.

Using Online Calculators for Precision

While manual calculations help you understand the math, online credit card payoff calculators give you precise timelines in seconds. These tools account for compound interest and provide exact payoff dates.

Most calculators ask for:

- Your current credit card balance

- Your interest rate (APR)

- Your planned monthly payment

- Any additional one-time payments you can make

Popular free calculators include those offered by Bankrate, NerdWallet, and CreditKarma. Simply input your information, and you’ll see not only when you’ll be debt-free but also how much you’ll pay in total interest.

Many calculators also show you alternative scenarios—for example, what happens if you increase your payment by $50 or $100. This feature is incredibly motivating because you can see exactly how small changes create big results.

Factors That Speed Up (or Slow Down) Your Payoff Timeline

Understanding what affects your timeline helps you make strategic decisions about your debt repayment.

Interest Rate: Your Biggest Enemy

Your APR has an enormous impact on how quickly you can pay off debt. The average credit card interest rate in the United States hovers around 20-24%, but rates can range from as low as 12% to as high as 29.99% depending on your creditworthiness and the type of card.

Higher interest rates mean more of your payment goes toward interest rather than reducing your actual debt. If you have a high APR, exploring balance transfer options or personal loans with lower rates could dramatically speed up your payoff timeline.

Payment Consistency Matters

Making consistent monthly payments is crucial, but life happens. Missing even one payment can trigger penalty APRs (sometimes as high as 29.99%), which can add months or even years to your payoff timeline. Setting up automatic payments ensures you never miss a due date.

New Charges Extend Your Timeline

Every time you add new charges to a card you’re trying to pay off, you’re extending your timeline. If you’re paying $300 monthly but charging $150 in new purchases, you’re only making $150 in progress. The most effective approach is to stop using the card entirely until it’s paid off.

Minimum Payment Adjustments

Credit card companies typically reduce your minimum payment as your balance decreases. While this feels like relief, it actually extends your payoff timeline if you adjust your payments downward. Keep paying the same amount (or more) even as your minimum decreases.

Proven Strategies to Pay Off Your Credit Card Faster

Now that you understand the timeline, let’s explore practical strategies to accelerate your progress.

The Snowball Method

This psychological approach focuses on momentum. List all your credit cards from smallest to largest balance. Make minimum payments on everything except the smallest balance, which you attack with all available funds. Once that’s paid off, roll that payment into the next smallest balance.

While this doesn’t save the most money mathematically, it provides quick wins that keep you motivated. Paying off that first card feels amazing and builds confidence that you can eliminate the rest.

The Avalanche Method

This is the mathematically optimal approach. List your cards from highest to lowest interest rate. Focus all extra payments on the highest-rate card while making minimums on others. Once the highest-rate card is paid off, move to the next highest.

This method saves you the most money in interest over time, though it may take longer to experience that first “payoff win” if your highest-rate card has a large balance.

The Balance Transfer Strategy

If you have good credit, transferring your balance to a card with a 0% introductory APR period (typically 12-21 months) can save you substantial interest. During this promotional period, 100% of your payment goes toward principal.

The key is to pay off as much as possible before the promotional period ends. Be aware of balance transfer fees (usually 3-5% of the transferred amount) and make sure the savings outweigh the cost.

Increase Your Income Temporarily

Consider taking on a side hustle specifically to pay down credit card debt. Whether it’s freelancing, driving for a rideshare service, or selling items you no longer need, dedicating this extra income entirely to debt can cut your timeline in half.

Even an extra $200-300 monthly from a side income can transform a 5-year payoff into a 2-year journey.

Use Windfalls Strategically

Tax refunds, work bonuses, birthday money, or any unexpected income should go directly to your credit card balance. A single $1,000 payment on a $5,000 balance can shave months off your timeline.

Negotiate a Lower Interest Rate

This surprisingly effective tactic requires just a phone call. Contact your credit card company and ask for a lower APR. If you have a history of on-time payments, many companies will reduce your rate by several percentage points. This single conversation can save you hundreds or thousands of dollars.

Common Mistakes That Extend Your Payoff Timeline

Avoid these pitfalls that keep people in credit card debt longer than necessary.

Continuing to Use the Card

The biggest mistake is treating your credit card like a debit card while trying to pay it off. Each new charge restarts the interest clock on that amount. Put the card away—freeze it in a block of ice if you need to—until you’ve paid it off.

Only Paying the Minimum

We’ve discussed this throughout, but it bears repeating: minimum payments are designed to keep you in debt as long as possible. Always pay more than the minimum, even if it’s just an extra $25.

Ignoring the Root Cause

If overspending or emergency lack of savings led to credit card debt, paying off the card without addressing these issues means you’ll likely end up in debt again. Build a small emergency fund simultaneously and examine your spending habits.

Falling for “Debt Relief” Scams

Be wary of companies promising to eliminate your debt for pennies on the dollar or charging high upfront fees. Legitimate debt consolidation and credit counseling services exist, but many predatory companies make situations worse.

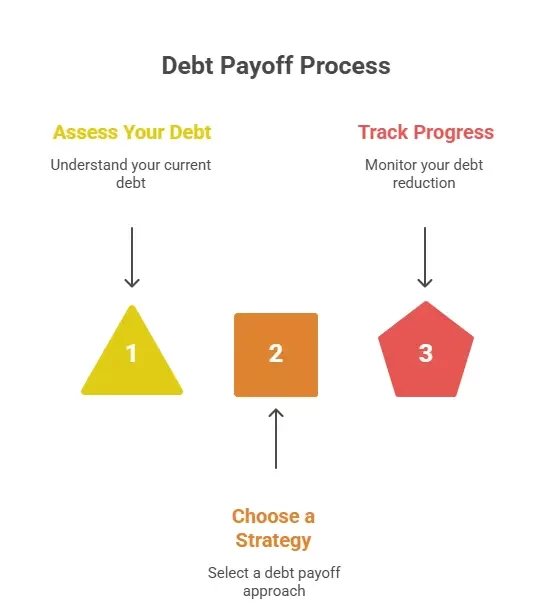

Creating Your Personal Payoff Plan

Now it’s time to create your customized strategy.

Step 1: Know Your Numbers Gather all your credit card statements and list out each card’s balance, interest rate, and minimum payment.

Step 2: Calculate Your Timeline Use an online calculator to see when you’ll be debt-free at your current payment rate, then run scenarios with higher payments.

Step 3: Determine What You Can Afford Review your budget honestly. Where can you cut expenses or increase income to put more toward debt?

Step 4: Choose Your Strategy Decide whether the snowball or avalanche method resonates more with your personality and financial situation.

Step 5: Set Up Automatic Payments Automate your payments to ensure consistency and avoid late fees that derail your progress.

Step 6: Track Your Progress Create a visual tracker—whether a spreadsheet, app, or chart on your wall—to see your balance decrease. This visibility keeps you motivated.

Step 7: Celebrate Milestones When you pay off 25%, 50%, or 75% of your debt, acknowledge your progress. This journey requires discipline, and recognizing your achievements helps you stay committed.

Final Thoughts: Your Debt-Free Future Starts Now

Figuring out how long it will take to pay off your credit card isn’t just about math—it’s about taking control of your financial future. Whether your timeline is 6 months or 6 years, the most important step is starting today with a clear plan.

Remember that the timeline isn’t set in stone. Every extra dollar you pay reduces both the time and the total interest you’ll pay. Small consistent actions compound into major results. That $5,000 balance might seem overwhelming today, but with a solid strategy and commitment, you’ll be celebrating your debt-free status sooner than you think.

The difference between someone who stays in credit card debt for decades and someone who becomes debt-free in a few years isn’t income—it’s intentionality. Now that you understand exactly how payoff timelines work and have proven strategies to accelerate your progress, you have everything you need to create your own success story.

Take out a calculator, run your numbers, and commit to your first action step today. Your future debt-free self will thank you for the decision you make right now.