Debt-Free Journey: How to Crush Your Loans Faster

Imagine waking up one morning with zero debt hanging over your head. No more anxious nights calculating minimum payments, no more choosing between savings and loan obligations, and no more feeling trapped by financial decisions you made years ago. This isn’t just a dream—it’s a reality thousands of Americans achieve every year, and you can too.

Whether you’re drowning in student loans, credit card debt, or car payments, the path to becoming debt-free is clearer than you think. In this comprehensive guide, we’ll walk you through proven strategies that have helped real people eliminate their debt years ahead of schedule. By the end of this article, you’ll have a personalized action plan to accelerate your debt payoff and reclaim your financial freedom.

[Image placeholder: Inspirational graphic showing a person climbing a mountain made of coins, reaching toward a debt-free summit with rays of sunlight breaking through clouds above]

Why Your Debt-Free Journey Starts with Understanding Your Numbers

Before you can crush your loans faster, you need to know exactly what you’re dealing with. Many people avoid looking at their total debt because it feels overwhelming, but this is the most critical first step. Think of it like getting on a scale before starting a fitness journey—you need a baseline to measure your progress.

Calculate Your Total Debt Load

Grab a notebook or open a spreadsheet and list every debt you owe:

- Student loans (federal and private)

- Credit card balances (all cards, even small amounts)

- Auto loans

- Personal loans

- Medical debt

- Home equity loans or lines of credit

For each debt, write down three key numbers: the total balance, the interest rate, and the minimum monthly payment. This exercise alone puts you ahead of 40% of Americans who don’t know their exact debt numbers.

Once you see everything in one place, calculate your debt-to-income ratio. Simply divide your total monthly debt payments by your gross monthly income and multiply by 100. If your ratio is above 43%, lenders consider you heavily burdened, and this should be your wake-up call to take aggressive action.

The Two Proven Methods to Pay Off Debt Faster

Financial experts have identified two primary strategies for accelerating debt payoff, and both work—the key is choosing the one that matches your personality and motivation style.

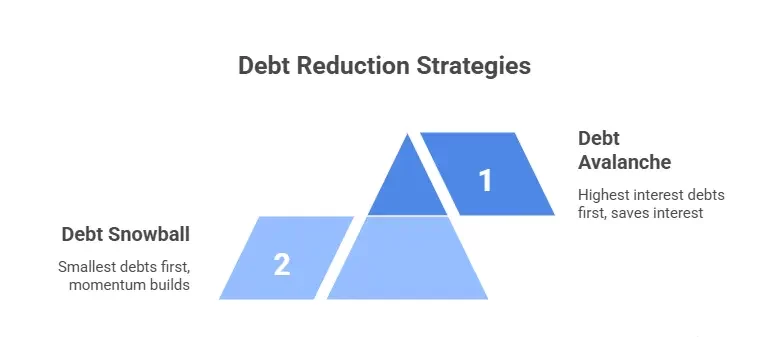

The Debt Snowball Method: Psychology Over Math

The debt snowball method prioritizes paying off your smallest debts first, regardless of interest rate. Here’s why it works: humans are motivated by quick wins. When you eliminate a debt completely within weeks or months, you get a psychological boost that keeps you committed to the journey.

How to implement the debt snowball:

- List all your debts from smallest to largest balance

- Make minimum payments on everything except the smallest debt

- Attack the smallest debt with every extra dollar you can find

- Once it’s paid off, take that payment amount and add it to the minimum payment of the next smallest debt

- Watch your payment snowball grow as you eliminate each debt

Sarah from Ohio used this method to pay off $32,000 in debt in just 18 months. “Paying off my first credit card with a $800 balance in six weeks gave me the confidence that I could actually do this,” she shares. “That momentum carried me through paying off much larger debts.”

The Debt Avalanche Method: Maximum Interest Savings

If you’re motivated by numbers and logic, the debt avalanche method will save you the most money in interest charges. With this approach, you target your highest-interest debt first while making minimum payments on everything else.

How to implement the debt avalanche:

- List all debts from highest to lowest interest rate

- Put all extra money toward the debt with the highest rate

- Once it’s eliminated, roll that payment into the debt with the next highest rate

- Continue until all debts are paid

Michael from Texas saved $4,200 in interest by using the avalanche method on his credit card debt. “I knew mathematically this was the smartest choice,” he explains. “Seeing how much interest I was avoiding kept me motivated even when progress felt slow.”

How to Find Extra Money to Crush Your Debt

You’ve chosen your payoff strategy, but now comes the crucial question: where do you find extra money to accelerate your payments? The answer lies in both increasing your income and cutting expenses strategically.

The 50/30/20 Budget Reallocation

Start by examining your current spending through the 50/30/20 framework: 50% on needs, 30% on wants, and 20% on savings and debt. If you’re serious about becoming debt-free faster, temporarily shift to a 50/20/30 split, redirecting 30% toward debt elimination.

This doesn’t mean eliminating all joy from your life. Instead, it means making intentional choices. That $150 monthly subscription bundle? Trim it to $50. The daily $6 coffee? Make it a twice-weekly treat. These aren’t permanent sacrifices—they’re strategic moves that can shave years off your debt timeline.

Earn More Money (Even with Limited Time)

Increasing your income creates the fastest path to debt freedom because there’s no ceiling on how much you can earn, unlike expenses which can only be cut so far.

Quick income boosters that work:

- Freelance your existing skills on platforms like Upwork or Fiverr (writing, design, consulting)

- Sell items you don’t use through Facebook Marketplace or eBay (aim for $500-$1,000)

- Pick up a part-time gig doing food delivery, rideshare, or retail (even 10 hours weekly adds up)

- Ask for a raise at your current job with documented value you’ve provided

- Turn hobbies into income like photography, baking, or tutoring

Jennifer from California added $800 monthly by freelancing graphic design just 5 hours per week. “Every penny went straight to debt,” she says. “Within 11 months, I’d eliminated $8,800 in credit card balances.”

Advanced Strategies to Accelerate Your Debt Payoff

Once you’ve mastered the basics, these powerful techniques can turbocharge your progress and potentially cut years off your debt timeline.

The Balance Transfer Hack

If you have good credit (scores above 670), balance transfer credit cards offering 0% APR for 12-21 months can be game-changers. By transferring high-interest credit card debt to a 0% card, every dollar you pay goes toward principal, not interest.

Important considerations: Most cards charge a 3-5% transfer fee, so do the math to ensure you’ll save more than the fee costs. More critically, you must pay off the balance before the promotional period ends, or you’ll face high interest rates on the remaining balance.

Refinancing and Consolidation

For student loans and personal loans, refinancing to a lower interest rate can save thousands while simplifying your payments. If you have federal student loans, however, weigh this carefully—refinancing with a private lender means losing federal protections like income-driven repayment plans and potential forgiveness programs.

Debt consolidation loans combine multiple debts into one payment, often at a lower interest rate. This works best when you’re consolidating high-interest credit card debt into a lower-rate personal loan, and you commit to not running up new credit card balances.

The Bi-Weekly Payment Strategy

Instead of making one monthly payment, split it in half and pay every two weeks. You’ll make 26 half-payments yearly (13 full payments) instead of 12 monthly payments. This extra payment goes entirely toward principal, shaving months or years off your loan term.

For a $20,000 loan at 6% interest, this strategy alone could save you $1,400 and eliminate the debt 2 years earlier. Set up automatic payments aligned with your paychecks so you never have to think about it.

Negotiate Lower Interest Rates

Many people don’t realize that credit card companies will sometimes lower your interest rate just by asking. Call your card issuer, explain that you’re a good customer working to pay down debt, and request a rate reduction. Mention competitive offers you’ve received.

Even dropping from 22% to 18% APR on a $5,000 balance saves you hundreds of dollars and accelerates payoff. The worst they can say is no, but success rates for long-time customers with good payment history are surprisingly high.

Staying Motivated on Your Debt-Free Journey

Paying off debt isn’t a sprint—it’s a marathon that requires sustained motivation and mental resilience. The excitement of starting fades, and the middle months can feel discouraging. Here’s how to maintain momentum.

Track and Celebrate Progress

Create a visual debt tracker that you see daily. Some people color in a thermometer-style chart, others cross off debts on a poster, and some use apps with progress bars. The visual reinforcement of watching your debt shrink keeps your goal tangible.

Celebrate milestones that aren’t just debt-related. After three months of consistent extra payments, treat yourself to a free activity you enjoy. When you hit the halfway point, have a modest celebration dinner. These small acknowledgments prevent burnout.

Find Your Accountability Partner

Share your debt-free goal with someone you trust—a friend, family member, or spouse. Schedule monthly check-ins to discuss progress, challenges, and wins. Knowing someone else is tracking your journey with you creates healthy accountability.

Online communities like Reddit’s r/DaveRamsey or r/personalfinance offer support from thousands of people on similar journeys. Reading success stories and getting advice during tough moments reminds you that you’re not alone.

Remember Your “Why”

When motivation wanes, reconnect with the deeper reason behind your debt-free goal. Is it financial security for your family? Freedom to pursue a career change? Ending the stress that keeps you awake at night? Write down your “why” and read it whenever you’re tempted to quit or overspend.

Common Mistakes That Slow Your Debt-Free Journey

Even with the best intentions, certain missteps can derail your progress. Avoid these common pitfalls that trap well-meaning people in prolonged debt.

Ignoring Emergency Savings

While it seems counterintuitive to save money while in debt, not having a small emergency fund (start with $1,000) means that unexpected expenses force you back into credit card debt. This creates a discouraging cycle where you feel like you’re making no progress.

Build your starter emergency fund first, then attack debt aggressively. Once debt-free, expand your emergency fund to 3-6 months of expenses.

Not Addressing the Root Cause

If overspending, emotional shopping, or lack of budgeting created your debt, simply paying it off won’t solve the problem. You’ll likely fall back into debt without addressing these underlying behaviors.

Work on your money mindset simultaneously with debt payoff. Read personal finance books, take a free online financial literacy course, or even consider working with a financial counselor if emotional spending is a significant issue.

Trying to Do Everything at Once

Some people get so excited about becoming debt-free that they slash their budget to unsustainable levels, work 70-hour weeks with multiple side hustles, and burn out within weeks. Sustainable progress beats aggressive short-term action that you can’t maintain.

Be realistic about what you can handle long-term. Even adding just $200 extra toward debt monthly makes a significant difference. Consistency over time beats sporadic intense efforts.

Your Next Steps to Debt Freedom

You now have the complete roadmap to accelerate your debt payoff and achieve financial freedom faster than you thought possible. The strategies in this guide have helped thousands of people eliminate debt years ahead of schedule—and they’ll work for you too.

Start today by taking these three immediate actions:

- Calculate your total debt and choose either the snowball or avalanche method based on your personality

- Find your first $100 in extra monthly payments by cutting one expense or adding a small income stream

- Set up automatic payments so your commitment doesn’t rely on willpower alone

Remember, becoming debt-free isn’t about perfection—it’s about progress. Some months you’ll crush your goals, and others you’ll barely maintain minimum payments. What matters is that you keep moving forward, learning from setbacks, and refusing to give up on your financial freedom.

Your debt-free journey starts right now, with this very next decision. Will you choose to take control of your financial future? The power has always been in your hands—now you have the knowledge to use it.

Start crushing your loans today, and soon you’ll be sharing your own debt-free success story.