Can You Really Afford That Home? A Simple Mortgage Math Guide

You’ve found your dream home. The kitchen is perfect, the backyard is spacious, and you can already picture yourself hosting family dinners in that dining room. But before you fall completely in love, there’s one critical question you need to answer honestly: Can you actually afford it?

If you’re feeling overwhelmed by mortgage calculators, confused about down payments, or worried about making a costly mistake, you’re not alone. According to recent data, nearly 40% of first-time homebuyers admit they didn’t fully understand the costs involved until after closing. The good news? Understanding mortgage affordability doesn’t require a finance degree—just some simple math and honest self-assessment.

In this comprehensive guide, we’ll break down exactly how to calculate what you can truly afford, uncover hidden costs most buyers miss, and give you a clear roadmap to confident homeownership. Let’s turn that anxiety into confidence with straightforward numbers anyone can understand.

Understanding the 28/36 Rule: Your First Reality Check

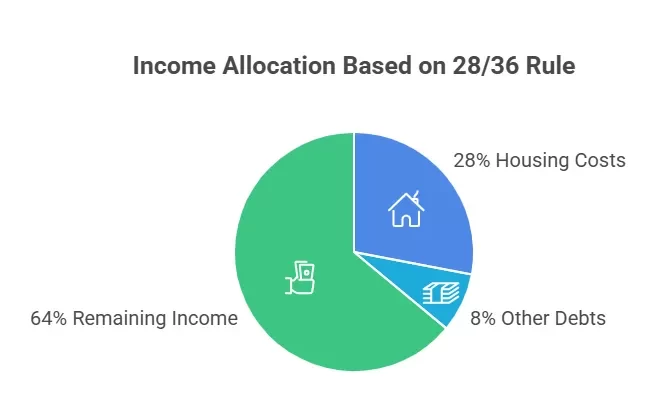

Before diving into complex calculations, let’s start with the golden rule that mortgage lenders use: the 28/36 rule. This simple formula has helped millions of Americans determine their home affordability boundaries.

Here’s how it works:

- 28% Rule (Front-End Ratio): Your total monthly housing costs shouldn’t exceed 28% of your gross monthly income

- 36% Rule (Back-End Ratio): Your total monthly debt payments (including housing) shouldn’t exceed 36% of your gross monthly income

Let’s make this real with an example. If you earn $75,000 annually:

- Your gross monthly income is $6,250

- Your maximum housing payment should be $1,750 (28% of $6,250)

- Your total debt payments shouldn’t exceed $2,250 (36% of $6,250)

This means if you already have $500 in monthly debt payments (car loan, student loans, credit cards), your maximum housing payment drops to $1,750 to stay within the 36% threshold.

Why these percentages? They’re based on decades of lending data showing that borrowers who exceed these ratios face significantly higher default risks. While some lenders may approve higher ratios, staying within these guidelines provides a crucial safety buffer for unexpected expenses.

The Four Components of Your True Monthly Housing Cost

Most first-time buyers make a dangerous assumption: they think their monthly mortgage payment equals their monthly housing cost. This is wrong—and it can sink your budget fast.

Your true monthly housing cost includes PITI + HOA, and understanding each component is essential:

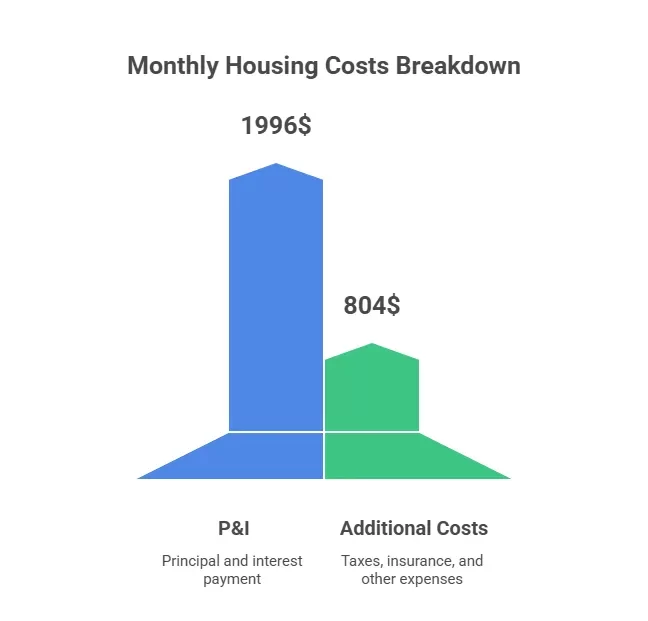

Principal and Interest (P&I)

This is the actual loan repayment. On a $300,000 mortgage at 7% interest for 30 years, your P&I payment would be approximately $1,996 monthly. Here’s what’s happening behind the scenes:

- Early years: Most of your payment goes toward interest (around $1,750 in month one)

- Later years: More goes toward principal, building your equity faster

- The shift: By year 15, your payments are roughly split 50/50 between principal and interest

Property Taxes

Property taxes vary dramatically by location, typically ranging from 0.5% to 2.5% of your home’s value annually. On a $300,000 home:

- Texas (1.8% average): $5,400 annually = $450 monthly

- California (0.76% average): $2,280 annually = $190 monthly

- Hawaii (0.28% average): $840 annually = $70 monthly

Critical tip: Property taxes can increase annually. Build in a 3-5% annual increase cushion when planning long-term affordability.

Homeowners Insurance

Insurance costs depend on your home’s value, location, age, and natural disaster risks. The national average is $1,428 annually ($119 monthly), but expect significantly higher costs if you’re in:

- Hurricane zones (Florida, Gulf Coast): $2,000-$4,000+ annually

- Earthquake zones (California): $800-$3,000+ annually

- Wildfire-prone areas (Western states): $1,500-$5,000+ annually

Private Mortgage Insurance (PMI)

If your down payment is less than 20%, you’ll pay PMI, typically 0.5% to 1% of the loan amount annually. On a $300,000 loan:

- 0.5% PMI: $125 monthly

- 1% PMI: $250 monthly

Good news: Once you reach 20% equity (through payments or appreciation), you can request PMI removal, potentially saving $1,500-$3,000 annually.

HOA Fees (If Applicable)

Homeowners Association fees range from $100 to $700+ monthly, depending on amenities and services. These fees typically cover:

- Exterior maintenance and landscaping

- Community amenities (pools, fitness centers)

- Trash collection and snow removal

- Building insurance (for condos)

Total Reality Check: That $300,000 home with a $1,996 P&I payment could actually cost you $2,700-$3,200 monthly when you include all PITI components and HOA fees.

The Down Payment Calculation: How Much Do You Really Need?

“You need 20% down to buy a home” is one of the most persistent—and misleading—myths in real estate. While 20% down offers significant advantages, it’s far from your only option.

Down Payment Options Explained

20% Down Payment (Conventional Gold Standard)

- Pros: No PMI, lower interest rates, stronger negotiating position, smaller loan amount

- Cons: Requires substantial savings ($60,000 on a $300,000 home)

- Best for: Buyers with strong savings who want the lowest monthly costs

10-15% Down (Conventional Middle Ground)

- Pros: More achievable savings goal, still demonstrates financial stability

- Cons: PMI required, slightly higher interest rates

- Best for: Buyers balancing savings timeline with market conditions

3-5% Down (Conventional Low Down Payment)

- Pros: Faster path to homeownership, preserves cash for emergencies

- Cons: Higher PMI, larger loan amount, stricter qualification requirements

- Best for: Strong income earners with solid credit but limited savings

3.5% Down (FHA Loan)

- Pros: Easier credit qualification (580+ credit score), affordable for first-timers

- Cons: Mortgage insurance required for loan lifetime (if under 10% down), upfront MIP of 1.75%

- Best for: Buyers with lower credit scores or limited savings

0% Down (VA/USDA Loans)

- Pros: No down payment required, competitive rates, no PMI

- Cons: Eligibility restrictions (veterans/rural areas), funding fees may apply

- Best for: Eligible veterans or rural property buyers

The Down Payment Trade-Off Analysis

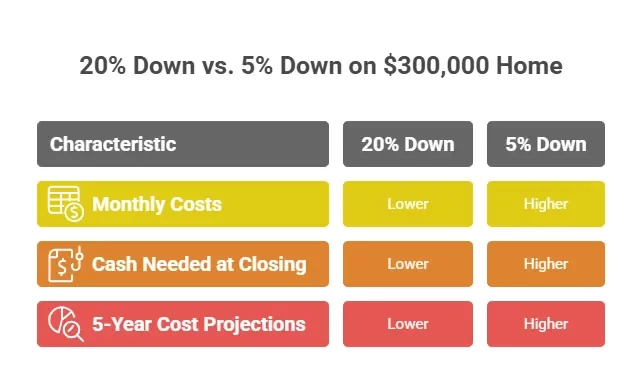

Let’s compare two scenarios on a $300,000 home purchase:

Scenario A: 20% Down ($60,000)

- Loan amount: $240,000

- Monthly P&I (at 6.5%): $1,517

- Monthly PMI: $0

- Total monthly: $1,517

Scenario B: 5% Down ($15,000)

- Loan amount: $285,000

- Monthly P&I (at 7%): $1,896

- Monthly PMI: $237

- Total monthly: $2,133

The difference is $616 monthly, or $7,392 annually. However, Scenario B preserves $45,000 in cash reserves for emergencies, repairs, or investments. The right choice depends on your complete financial picture, not just the monthly payment.

The Hidden Costs That Destroy Budgets

Even financially savvy buyers underestimate these often-overlooked expenses that can add thousands to your homeownership costs:

Closing Costs (2-5% of Purchase Price)

On a $300,000 home, expect $6,000-$15,000 in closing costs, including:

- Loan origination fees: $1,500-$3,000

- Appraisal: $400-$600

- Title insurance: $1,000-$2,000

- Attorney fees: $500-$1,500

- Home inspection: $300-$500

- Prepaid property taxes and insurance: Variable

Pro tip: Many buyers negotiate seller credits to cover closing costs, effectively reducing your cash needs by thousands.

Move-In Costs ($5,000-$15,000+)

The first few months are expensive:

- Moving services: $1,000-$5,000

- Furniture and appliances: $2,000-$8,000

- Window treatments and basics: $1,000-$3,000

- Utility deposits and setup: $500-$1,000

- Immediate repairs or updates: $1,000-$5,000+

Ongoing Maintenance (1-2% Annually)

The often-repeated rule is to budget 1-2% of your home’s value annually for maintenance and repairs. On a $300,000 home, that’s $3,000-$6,000 yearly ($250-$500 monthly).

Common unexpected expenses in year one:

- HVAC service or repair: $150-$5,000

- Plumbing emergencies: $200-$1,000

- Appliance replacement: $400-$2,000

- Roof repairs: $300-$3,000

- Pest control: $100-$500

Utility Increases

Expect utility costs to increase significantly from renting:

- Apartment (800 sq ft): $100-$150 monthly average

- Single-family home (2,000 sq ft): $200-$400 monthly average

Older homes, poor insulation, and extreme climates can push utilities to $500-$800+ monthly.

Your Step-by-Step Affordability Calculation

Mortgage Calculator

Now let’s put everything together with a practical, fill-in-the-blanks calculation you can do right now.

Step 1: Calculate Your Maximum Housing Budget

Your gross monthly income: $_________ Multiply by 0.28: $_________ This is your maximum monthly housing payment (PITI + HOA)

Step 2: Subtract Your Existing Debts

Your current monthly debt payments (car, student loans, credit cards): $_________ Your gross monthly income × 0.36: $_________ Subtract your current debts from the 36% figure: $_________ This is your maximum housing payment if you have existing debt

Use the lower number from Steps 1 and 2 as your ceiling.

Step 3: Estimate Your Full PITI + HOA

Based on homes you’re considering:

- Property taxes (monthly estimate): $_________

- Homeowners insurance (monthly): $_________

- HOA fees (if applicable): $_________

- PMI (if down payment under 20%): $_________

Add these together: $_________

Step 4: Calculate Available for P&I

Your maximum housing budget (from Step 2): $_________ Minus your estimated taxes, insurance, HOA, PMI: $_________ This is what you have available for principal and interest

Step 5: Determine Your Home Price Range

Use an online mortgage calculator and work backwards. Input your available P&I amount, expected interest rate, and 30-year term to find your maximum loan amount.

Add your down payment to find your maximum home price.

Example Calculation:

- Gross monthly income: $6,000

- Maximum housing (28%): $1,680

- Existing debt: $400

- Available housing budget (36% rule): $1,760

- Use $1,680 (lower amount)

- Estimated taxes, insurance, PMI: $530

- Available for P&I: $1,150

- At 7% interest, $1,150 monthly = approximately $172,000 loan

- With 10% down ($19,000), maximum home price: $191,000

The Affordability Reality Check: Questions to Ask Yourself

Numbers tell part of the story, but honest self-reflection completes the picture. Before committing, ask yourself:

Financial Stability Questions

1. Do I have 3-6 months of expenses saved beyond my down payment? Homeownership brings unexpected costs. Emergency funds are non-negotiable.

2. Is my income stable and likely to remain so? New job? Commission-based? Self-employed? Build extra cushion into your budget.

3. Am I planning other major life changes in the next 2-3 years? Marriage, children, career changes, or relocations may impact affordability.

4. Can I afford this home if interest rates rise when I refinance? If you’re considering an adjustable-rate mortgage, model worst-case scenarios.

Lifestyle Questions

1. Will I still be able to save for retirement? Financial advisors recommend continuing to save 10-15% of income even after buying.

2. Can I maintain my current lifestyle? Calculate how homeownership will impact dining out, travel, hobbies, and entertainment.

3. Am I comfortable with the maintenance responsibilities? Time and money are required. Are you prepared for both?

4. Is this home serving a 5+ year need? With closing costs and appreciation timelines, shorter ownership periods often lose money.

Common Mortgage Math Mistakes to Avoid

Learn from these frequent errors that trip up even smart buyers:

Mistake #1: Maxing Out Your Approval Amount

Lenders approve you based on risk tolerance—not your happiness. Just because you’re approved for $400,000 doesn’t mean you should spend it. Most financial experts recommend staying 20-25% below your maximum approval to preserve quality of life.

Mistake #2: Forgetting About Tax Changes

Homeownership changes your tax situation. While mortgage interest is deductible, the increased standard deduction means many homeowners no longer itemize. Don’t count on massive tax savings that may not materialize.

Mistake #3: Ignoring Your Partner’s Debt-to-Income Ratio

When applying jointly, both incomes AND both debts are considered. Your partner’s student loans or car payment directly impact your home affordability.

Mistake #4: Assuming Appreciation Will Save You

While home values generally increase long-term, short-term dips happen. Never buy a home you can’t afford today hoping appreciation will bail you out.

Mistake #5: Depleting All Savings for the Down Payment

That 20% down payment isn’t worth it if you’re left with $500 in the bank. Preserve emergency funds, moving costs, and immediate repair budgets.

Your Action Plan: Next Steps to Smart Homeownership

You’ve done the math—now what? Follow this practical roadmap:

Immediate Actions (This Week):

- Complete the five-step affordability calculation above with your real numbers

- Check your credit score (free at annualcreditreport.com)

- Gather six months of pay stubs and bank statements

- List your current monthly debts with exact payment amounts

Short-Term Actions (This Month):

- Get pre-approved by 2-3 lenders to compare rates and terms

- Research property tax rates in your target neighborhoods

- Get homeowners insurance quotes for your price range

- Build a realistic budget showing your current spending vs. post-purchase spending

Before You Start House Hunting:

- Establish your non-negotiable maximum price (not your approval amount)

- Save additional emergency funds beyond your down payment

- Improve your credit score if below 740 (even 20 points can save thousands in interest)

- Pay down high-interest debt to improve your debt-to-income ratio

During the Home Search:

- Request detailed property tax history and HOA financials for every serious contender

- Get homeowners insurance quotes for specific addresses before making offers

- Budget for a thorough home inspection ($400-$600 well spent)

- Run your affordability calculation for each specific property—don’t assume all homes in your range cost the same monthly

Conclusion: Confidence Comes from Clarity

The question “Can you really afford that home?” doesn’t have to feel overwhelming. With the simple mortgage math you’ve learned today, you now have the tools to answer honestly and confidently.

Remember these key takeaways:

- Use the 28/36 rule as your foundation, not your lender’s maximum approval

- Calculate total PITI + HOA costs, not just the principal and interest

- Preserve emergency funds beyond your down payment—homeownership brings surprises

- Account for hidden costs like maintenance, utilities, and move-in expenses

- Choose a payment that allows you to live, not just survive

Homeownership is one of life’s greatest milestones and wealth-building tools—but only when you buy within your true means. The math doesn’t lie, and now you know exactly how to run the numbers.

Your dream home is out there, and with this knowledge, you’ll recognize it not just by how it makes you feel, but by how comfortably it fits your budget. That’s when a house truly becomes a home worth buying.

Ready to take the next step? Save this guide, complete your personal calculations, and approach your home search with the confidence that comes from knowing your numbers inside and out. Your future self will thank you for doing the math today.