Is My Emergency Fund Sufficient? A Complete Guide to Financial Security

You’ve been diligently setting aside money each month, watching your emergency fund grow. But as you stare at that balance, a nagging question keeps surfacing: is it actually enough? Let’s dive deep into understanding whether your emergency fund can truly protect you when life throws its inevitable curveballs.

What Makes an Emergency Fund “Sufficient”?

An emergency fund is your financial safety net, designed to cover unexpected expenses or income loss without forcing you to rely on credit cards or loans. But sufficiency isn’t a one-size-fits-all concept—it depends entirely on your unique circumstances.

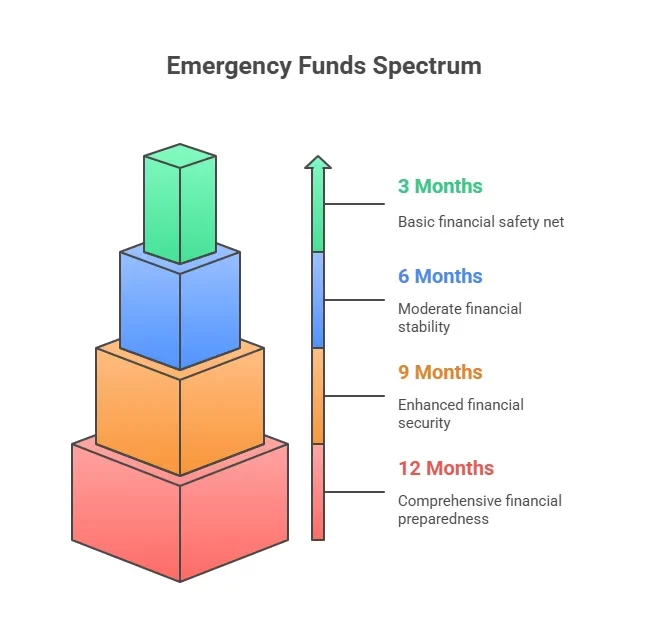

The Traditional 3-6 Month Rule: Does It Still Apply?

[IMAGE: Infographic showing a spectrum/scale from 3 months to 12 months with different scenarios marked along it]

You’ve probably heard the standard advice: save three to six months of living expenses. While this remains a solid baseline, it’s just the starting point. Think of it as the foundation of a house—necessary, but not the complete structure.

Here’s when three months might work:

- You have dual incomes in your household

- Your job is stable with low layoff risk

- You have minimal debt obligations

- You’re in excellent health with good insurance coverage

Consider six months or more if:

- You’re the sole income earner

- You work in a volatile industry or as a freelancer

- You have dependents relying on your income

- You have chronic health conditions

- You own a home (hello, unexpected repairs!)

Calculating Your True Emergency Fund Need

Let’s get practical. Grab a calculator and let’s figure out your actual number.

Step 1: Calculate Your Monthly Essential Expenses

Start by listing only the expenses you absolutely cannot avoid:

Sarah’s Example:

- Rent/Mortgage: $1,200

- Utilities (electric, water, internet): $180

- Groceries: $400

- Insurance (health, auto, home): $350

- Car payment: $300

- Minimum debt payments: $250

- Basic transportation costs: $100

Sarah’s monthly essentials: $2,780

[IMAGE: Simple pie chart or bar graph showing the breakdown of Sarah’s monthly essential expenses with clear labels and amounts]

Notice what’s NOT included? Streaming services, dining out, gym memberships, and shopping. During a true emergency, these are the first to go.

Step 2: Apply Your Personal Multiplier

Now multiply your monthly essentials by your appropriate timeframe:

Sarah’s scenario: She’s a marketing professional in a stable company, married with one income, and has no major health issues. She calculates:

- Conservative approach: $2,780 × 6 months = $16,680

- Comfortable target: $2,780 × 9 months = $25,020

Sarah decides to aim for $20,000—seven months of coverage—as her sweet spot.

The Hidden Factors That Change Everything

Beyond the basic calculation, several factors can dramatically impact whether your emergency fund is truly sufficient.

Your Job Security Reality Check

Be honest with yourself about your employment situation. If you work in tech, journalism, or retail—industries known for sudden layoffs—you need more cushion. Industry research shows the average job search takes 3-5 months, but in specialized fields or during economic downturns, it can stretch to 6-9 months.

Real-world example: Michael, a software engineer, kept six months saved ($18,000). When his company downsized, he assumed he’d find work quickly given his skills. Six months later, still job hunting, he burned through his entire fund and had to borrow from family for month seven. He now maintains a 12-month emergency fund.

The Home Ownership Factor

Renters and homeowners face vastly different emergency scenarios. When Sarah rented, her $16,680 fund felt adequate. After buying a home, she experienced the harsh reality: a failed HVAC system in summer ($6,500), a roof leak ($3,200), and a water heater replacement ($1,800)—all within 18 months.

Homeowner adjustment: Add $5,000-$10,000 to your target specifically for home repairs, or maintain a separate home maintenance fund.

The Gig Economy and Variable Income Challenge

If you’re self-employed, a freelancer, or work on commission, your emergency fund needs to work harder. Not only do you face income volatility, but you also lack unemployment benefits.

Recommended multiplier for variable income: 9-12 months of expenses, minimum.

Signs Your Emergency Fund Isn’t Sufficient

Watch for these red flags:

- You’re anxious about money constantly. If your fund doesn’t bring peace of mind, it’s not enough for your psychological comfort—and that matters.

- You’ve dipped into it multiple times this year. This suggests either your fund is too small or you need better budgeting for predictable irregular expenses (car insurance, holiday gifts, etc.).

- One emergency would wipe it out. If a single job loss or medical event would completely drain your fund, you need more.

- Your life circumstances have changed. Had a baby? Bought a house? Started a business? Your old fund target is now obsolete.

Building Your Fund: Practical Action Steps

Knowing you need more is one thing; getting there is another. Here’s how to bridge the gap:

The Percentage Approach

Rather than feeling overwhelmed by a large target, commit to a percentage of each paycheck:

- Minimum: 10% of net income

- Aggressive: 20% of net income

- Extreme savings mode: 30%+ of net income

Example: On a $4,000 monthly take-home, saving 15% means $600 monthly toward your emergency fund. At this rate, you’d reach $20,000 in about 33 months (just under 3 years).

Front-Load Your Fund

Use these opportunities to supercharge your savings:

- Tax refunds

- Work bonuses

- Cash gifts

- Side hustle income

- Unexpected windfalls

When Sarah received a $3,500 tax refund, putting it directly into her emergency fund immediately boosted her timeline by six months.

The Two-Account Strategy

Keep your emergency fund in a high-yield savings account—separate from your checking account. This creates a psychological barrier against casual spending while earning you interest (currently 4-5% APY at many online banks).

Pro tip: Make it slightly inconvenient to access. A transfer that takes 1-2 business days prevents impulsive withdrawals.

When to Reassess Your Emergency Fund

Your emergency fund isn’t a “set it and forget it” situation. Schedule a review every:

- Six months during stable periods

- Immediately after major life changes (marriage, divorce, new baby, home purchase)

- When you change jobs or income sources

- After you use the fund (to determine why and prevent future dips)

The Bottom Line: Is Yours Sufficient?

Here’s your personal emergency fund sufficiency checklist:

✅ Covers 3-12 months of essential expenses (based on your situation)

✅ Includes buffer for home repairs if you own property

✅ Accounts for your income stability and job market

✅ Provides genuine peace of mind, not just a number

✅ Lives in an accessible but separate savings account

✅ Gets reviewed and adjusted regularly

If you checked all these boxes, congratulations—your emergency fund is likely sufficient. If not, you now have a clear roadmap for getting there.

Remember, building an emergency fund is a marathon, not a sprint. Every dollar you save is a dollar of security, stress reduction, and freedom. Start where you are, be consistent, and adjust as your life evolves. Your future self will thank you for the financial cushion you’re building today.

What’s your next step? Calculate your personal emergency fund target right now, then set up an automatic transfer for your first (or next) contribution. Small actions today create significant security tomorrow.